RetailWise Team has recently visited Singapore, and we’re thrilled to dive into its most innovative retail destinations! This week, we’ll be showcasing standout retailers with unique features and concepts.

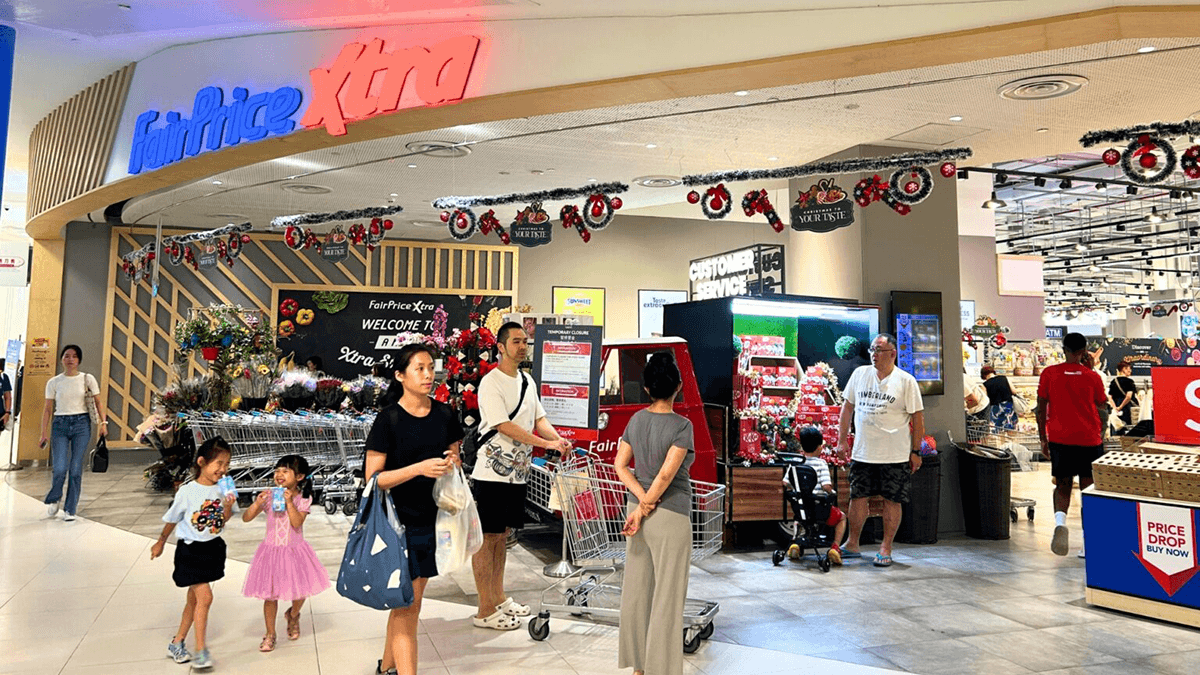

First up: FairPrice Xtra at VivoCity

With an impressive 90,000 sq ft of retail space, including Unity Pharmacy on the second floor, this is the largest Fairprice store in Singapore.

What makes this store even more remarkable is that customers are greeted by a vibrant, expansive display of fresh fruits and vegetables, setting the tone with a burst of color and freshness right at the store entrance. Every visitor will find freshly delivered produce daily. They offer hydroponically grown vegetables harvested on-site, bringing farm-to-table right into the heart of the store!

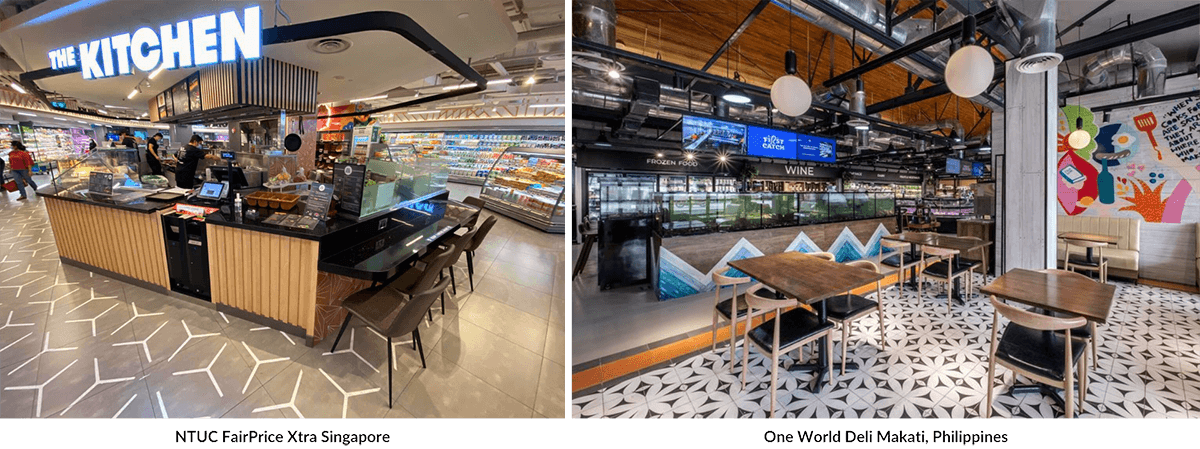

The unique experiences don’t end there. Fairprice Xtra has a dining area at the core of the store, featuring zones like ‘Pick, Prep, Enjoy,’ and ‘The Kitchen,’ offering ready-to-eat meals, a dedicated sushi and sashimi area, cold cuts, pre-cut fruits, and an on-demand grill where you can select seafood or meat and have them prepared just the way you like. During our visit, we indulged in the ‘Oyster and Wine Night,’ enjoying fresh French oysters paired perfectly with wine.

The store’s layout is well-designed, with a spacious seafood section featuring farmed fish, live Dungeness crabs, and a variety of shellfish. The butchery area boasts premium selections, including grass-fed and grain-fed beef from Australia and New Zealand, catering to quality-conscious shoppers.

Fairprice Xtra also caters a have a beautiful bakery area with a wide selection of breads and pastries, a cozy café with seating area, dairy, and chilled sections. Fairprice Xtra truly is a one-stop shopping experience.

The second floor expands offerings with International and Local favorites, Sports & Leisure, Travel Essentials, Beauty & Wellness, Electronics, Home & Living, Mums & Kids, Pet Care, and Wines, Beer & Spirits.

This hypermarket exemplifies retail excellence, remaining fully stocked and organized even late into the evening, with self-service stations for weighing fruits and quick checkouts. Opened in 2019, this store is built around customer convenience and sustainability. Shoppers can have food prepped for easy home cooking, buy loose quantities of grains and nuts, and explore over 35,000 products, including 350+ local brands. A dedicated corner supports local enterprises, reinforcing FairPrice’s commitment to sustainability and customer-focused innovation. Stay tuned for more highlights from our Singapore retail journey as we continue to explore some of the city’s most inspiring retail experiences.

At RetailWise, we are bringing value across different brands. We aim to ensure your satisfaction by guaranteeing the success of your business from strategy to execution. Explore our strategies, resources, and expertise and find the perfect fit for your needs click here

I vividly remember the excitement of visiting the newest and closest hypermarket to our municipality in France with my aunt and uncle. These visits, once or twice a month on Tuesdays, were a highlight since I had no school on Wednesdays. My first stop was always the books section, where I would lose myself in reading while waiting for them to finish their shopping. Afterwards, we would eat together at the mall’s cafeteria.

In the 1970s, the hypermarket concept was predominantly developed and promoted by retailers. These large stores, ranging from 10,000 to 15,000 square meters selling area, offered a wide variety of products under one roof – electronics, appliances, apparel, general merchandise, food, and non-food grocery items, along with a large fresh food area. The promise was a vast selection at affordable prices. However, this concept was controversial, posing a real threat to small independent businesses like meat shops, bakeries, and fruit and vegetable stores.

An Insightful Experience in the Hypermarket Business

Was it a coincidence that I began my professional career in the hypermarket business 15 years later? Starting in the retail industry, specifically in the hypermarket business with Auchan in 1988, was indeed a fantastic experience. Store operation managers were highly decisive in a decentralized organization, handling everything from buying to selling, with full accountability for their profit and loss statements.

Daily pep talks with the team and weekly reporting to the department head created a competitive environment for young managers. At that time, we were directly negotiating with supplier representatives, selecting promotions, and controlling daily orders.

Initiatives on planograms, coordinated with the centralized merchandise team, were welcomed. Buyers were gathering regular information on categories and products through constant communication with store operations personnel.

Our time was clearly divided between store preparation before opening and during the “re-opening” before the evening rush, administrative tasks, and supplier negotiations. Most importantly, constant communication and interaction with the store team were critical. Store personnel provided valuable feedback for young managers, benefiting from their extensive field experience and daily customer interactions.

I remember the regular sales challenges introduced by management, where we would arrive early to display our promotions extravagantly. Competition was fierce among the young managers (read: wolves!) to conquer challenges, and our creativity in showcasing the most impressive and innovative displays seemed limitless.

The principle of the concept was simple: “Low prices, strong promotions, everything under one roof, spacious cash counter lines, and ample parking to accommodate heavy customer traffic.” We felt invincible, anticipating that hypermarkets would gradually replace supermarkets and neighborhood stores. Back in the 1990s, the impact was indeed significant.

Today’s Reality: A Reflection on Decline

I travelled to Europe several times over the last three years and always made a point to visit stores, including hypermarkets. It was no different last August when I was in France and Spain. I have once again witnessed the continued decline of the hypermarket concept. There was so much space with few customers, empty cash counter lines, and a dark atmosphere – the excitement was gone.

Photo courtesy of Eric Poiret

Nevertheless, I must acknowledge the efforts made to maintain an outstanding fresh product offering with enticing displays, which still make a trip to the hypermarket worthwhile. The product selection is extensive, aiming to meet every customer’s request, even for niche items. The sheer volume on display, particularly the fish section, is impressive and tempting.

The option to choose between over-the-counter and pre-packed meat and fish is also a smart approach. The aroma of freshly baked bread and the remarkable pastry selection are highlights. The deli and cheese corner remain exciting, offering an amazing range from all over the world. New concepts, like the sushi bar and café corner, where you can have a quick breakfast or lunch with a variety of pastries and sandwiches, add a modern touch.

However, for dry food and personal care items, I see limited value. The product range is vast, but the display is uninteresting, and finding specific categories and merchandise can be challenging. There is nothing new, except perhaps the wine bar with a sommelier, and an expanded health and wellness section for the health-conscious.

For non-food items, primarily general merchandise, electronics, and apparel, there have been no significant changes or improvements in 30 years. While there are new products, the overall concept has not evolved and has even degraded in terms of attractiveness

What Happened Over The Years?

This decline is not without reason, as several factors have contributed to the hypermarket concept’s challenges, including shifts in market trends, consumer behavior, and increased competition.

Neighborhood Stores: Small supermarkets and compact hypermarkets have regained relevance. Economic considerations like rising transportation costs and a desire for more convenient shopping have favored proximity stores. Retail chains have also improved their smaller formats to offer almost everything, including fresh products and basic general merchandise, close to home. City stores in large urban areas effectively maximize small spaces to meet a wide range of needs, including fresh food and non-food categories, delivered right to your doorstep.

Specialty Stores: These stores have gained success by offering better assortments and prices in more enticing environments.

E-commerce and the Pandemic: The pandemic was a defining moment for hypermarkets. Modern retailers were pioneers in platform solutions, but e-commerce competition became fierce. All retailers now offer online platforms, and some are more relevant online than in physical stores. Independent e-commerce platforms have also emerged, creating new competition, while online food delivery options have surged.

Demographic Shifts: Changes in demographics, such as the increase in smaller households and aging populations, influence shopping behaviors. Smaller households prefer more frequent, smaller shopping trips rather than large, infrequent ones that hypermarkets accommodate.

Sustainability Concerns: Consumers are becoming more conscious of the environmental impact of their shopping habits, favoring stores that promote local products, reduce waste, and have smaller carbon footprints. Hypermarkets, with their extensive supply chains, can struggle to align with these values.

What’s Next? Suggestions for the Future of Hypermarkets

Retail chains have a significant opportunity to regain confidence in the hypermarket format by cultivating a mindset open to adapting to evolving customer trends and expectations. Based on my global experience in the hypermarket business, here are a few suggestions to consider.

Reduce Space: The first impression upon visiting a hypermarket at present is that it is too big. I find it difficult to understand why retail chains have not downsized existing stores over the years. In an era where prime space is valued and large boxes are losing popularity, retail chains should re-evaluate their use of space and declining sales productivity, perhaps transforming parts of hypermarkets into mall spaces, specialty stores, or dining experiences.

Improve Ambiance: It is a well-known fact that the hypermarket is a cutting-edge retail concept; unfortunately many have not evolved in terms of ambiance and visual appeal. Lighting, tiling, and visual concepts have remained unchanged for decades, and the absence of ambient music contributes to an uninviting atmosphere. Today’s customers crave experiential shopping that engages their senses – what they see, hear, and smell. This may be the perfect time to visually rebrand and transform this concept into one that is more vibrant and appealing for customers.

Enhance Customer Experience: This is probably the biggest opportunity. Rethinking the customer journey and creating engaging experiences for shoppers is key.

Given the quality of fresh offerings, there is an opportunity to emphasize and/or add dining experiences within the store, where customers can enjoy freshly prepared meals from the products they selected. This approach would engage customers’ senses, creating a strong appeal. Although this concept exists internationally in some high-end supermarkets, European retail chains have yet to embrace it strongly. Themed regional dining experiences – such as Asian, Mediterranean, or Mexican – could be introduced. With their existing volume and sourcing capabilities, hypermarket operators can additionally offer attractive price points. The challenge lies in creatively integrating dining experiences into the store layout without compromising space, customer flow, or navigation.

Similarly, there is a rise in new coffee concepts. Most hypermarkets have a basic grab-and-go coffee corner, but transforming it into a vibrant coffee shop inside the store could enhance the shopping experience. The coffee shop could be integrated near the bakery but designed to stand out visually.

For non-food items, integrating a “store within a store” concept could be beneficial. For example, Auchan could consider including a mini-Decathlon within the hypermarket, offering an immersive experience by inviting customers to try sports items in a dedicated zone.

For the electronics department, there is much room for rekindling excitement. I was once the head of this department, where customers would station themselves during home theater displays, showcasing the latest movies or concerts, with music resonating from afar. Surprisingly, during one of my hypermarket visits last August, I noticed that the TV units were switched off. While technology has evolved and most features are available in a single device, customers still desire to test and play with gadgets. Creating an engaging environment could attract customers and ultimately increase sales.

For apparel, collaborating with popular brands to create customized collections for the hypermarket could engage younger generations and revitalize the department’s offerings. These brands would have to ensure that price points remain accessible while maintaining the integrity of the concept.

Many of these suggestions have already been implemented in some modern retail chains worldwide. However, the necessary transformations in European markets appear to be occurring at a sluggish pace. Maintaining the status quo will only contribute to further decline. There is an opportunity to adapt to evolving market conditions and implement essential upgrades. Aesthetic changes alone may not be enough; a fundamental revolution in the hypermarket concept might be necessary. Benchmarking against successful markets in the US and Southeast Asia could offer valuable insights for European retail chains.

Final Thoughts: Embracing Change in Hypermarkets

Reflecting on my early experiences with French hypermarkets, it’s bittersweet to witness the decline of a concept that once promised a vibrant shopping experience under one roof. The memories of bustling aisles filled with excitement contrast sharply with the empty spaces I now observe. As we look to the future, it’s clear that revitalizing the hypermarket model will require not only a keen understanding of evolving consumer preferences but also a commitment to innovative and engaging shopping experiences. By embracing change and adapting to modern trends, hypermarkets can hope to rekindle the passion they once inspired in shoppers like myself.

I hope these thoughts motivate you to explore new ideas in retail and collaborate to revive the excitement that once made the hypermarket concept very special.

Eric has a solid experience of more than 35 years in the management of retail chains in the Gulf Region, Asia and France. Before becoming the Chairman of ERE, he was Managing Director for Metro Gaisano, Chief Operating Officer for ASWAAQ, a Dubai Government-owned company, and Chief Executive Officer for MAF Carrefour KSA. Eric Poiret’s expertise lies in strategic planning and operations management. Eric continues to expand his expertise by permanently keeping up with market trends through various engagements and visiting different retail markets around the world.

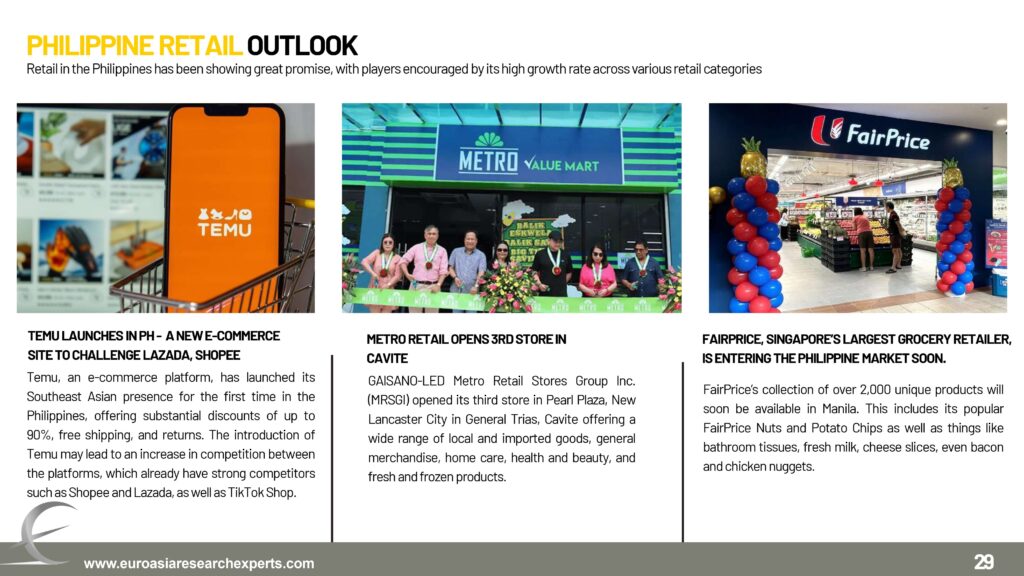

TikTok shopping is taking over Christmas shopping as the majority of TikTok users discover new brands and products for the season through the platform.

Move aside Jose Mari Chan, TikTok is growing to be synonymous with Filipino Christmas celebration and shopping this 2024. According to two studies commissioned by TikTok on Christmas and New Year behaviors of Filipinos, TikTok users are increasingly turning to the popular short video platform for community, entertainment and holiday TikTok shopping. With the growing dominance of the platform, it comes as no surprise that TikTok now occupies a central part in the Philippines’ biggest holiday.

A clearer picture of Filipino habits during the holiday season is emerging thanks to a 2024 report by research company Toluna. According to the report, 81% of TikTok users gather with friends and family, with 74% giving gifts, and 66% celebrating with Christmas parties.

Notably, shopping habits of Tiktok users have also been revealed. 60% of Filipino TikTok users reported spending time shopping for the season, with some doing so as early as September. In addition, according to a second report by Kantar Profile, 81% of Filipino TikTok users rely on the platform to discover new brands and products. And 77% of users go to TikTok to answer their shopping needs.

TikTok Shopping in Mega Sales Delight Shoppers

Tiktok’s Mega Sales are a prime driver for shopping on the TikTok platform. In the previous year, 84% of TikTok users were reported to have participated in these Mega Sales. This year, they are projected to increase their spending on TikTok by a factor of 2.3 times, compared to non-TikTok users. TikTok users are also expected to be 1.9 times more likely to spend more on Christmas gifts this year over the previous year.

This growth marks the emergence of TikTok as a preferred platform for shoppers during sales.

Paolo David, Philippine Brand and Partnerships Head at TikTok, said in a statement, “As the holiday season unfolds, TikTok continues to be a pivotal platform for Filipinos to celebrate Christmas. Whether it’s for discovery, entertainment, or shopping, TikTok offers a unique space where users can fully immerse themselves in the festive spirit. By understanding and engaging with the platform’s diverse shopping personas, brands can better position themselves to connect with a highly engaged audience, ensuring success throughout the holiday season and beyond.”

A Profile of Filipino TikTok Shoppers

Through the TikTok-commissioned study by Kantar Profile, a clearer picture of Filipino TikTok users is also emerging. The research company identified four distinct shopping personas from the study, which brands on the platform can use to generate insight and drive their marketing campaigns. The four personas of TikTok shoppers are:

Bargain Hunters

These users actively search for the best deals online and seek vouchers. 74% use TikTok more than once a day, and 78% shop weekly on various e-commerce platforms.

Inspirational Shoppers

For these users, shopping is an exploratory experience. They like to discover new brands and new shopping trends. 78% use TikTok daily, and 82% shop weekly. They are 1.2 times more likely to shop on social media.

Effortless Shoppers

These users make purchases for convenience, and prefer quick and easy shopping experiences. 73% use TikTok daily and 80% prefer hassle-free checkout.

Purposeful Shoppers

More considered than the other personas, these users like brands that align with their personal values, such as sustainability. 77% of them use TikTok more than once a day. They seek out brand-specific websites and are twice as likely to shop on these platforms.

Private labels first captured my attention as a child in the 70s during a visit to Cora, the newest hypermarket near my hometown in northern France. Amidst the bustling aisles filled with colorful packages, I was drawn to a section showcasing “white products” – merchandise packaged in plain, minimalistic white without branding. The store-brand products communicated their value clearly: unbranded and low-priced. This early encounter with private labels, offering significant savings despite their lack of flashy branding, piqued my ongoing interest in private labels as I journeyed into retail.

Key Insights in Private Label Development

When I began my retail career in 1988 at Auchan in France, private labels were quite different from what we see today. Back then, their packaging often mimicked that of leading brands to the point where it could confuse customers, despite private labels being priced about 20% lower.

From those early experiences, I picked up three key insights:

Identify the top brands in your category to effectively position your private label.

Set your private label’s price 20% lower than the leading brands to attract price-sensitive customers.

Ensure your private label offers a margin that is 15 to 20% higher than the category leader to ensure profitability.

A decade later, at Monoprix-Prisunic, I encountered the concept of exclusive premium retail brands – high-quality products that resonated with customers and helped differentiate the retailer.

In the Middle East with Carrefour, I faced the challenge of launching private labels in a market dominated by established international brands. Despite Carrefour’s global reach, our progress was slower than expected due to limited initial volumes.

At Aswaaq, the challenge was even greater as we had to develop a private label before the first supermarket had even opened, with minimal volumes to start. We chose to focus on ten basic commodities, targeting the low-price segment with a distinctive brand name.

Since moving to the Philippines in 2011, I have had three key experiences developing or enhancing private labels. Although private label sales remain relatively low at below 5% share of sales compared to Europe, which has a 30% to 40% share of sales, or the US, with a 25% share of sales, the rise of hard discounters like Dali and O!Save, and the “No Brand” concept with strong private label strategies, has pushed local retailers to reassess their approaches to private label development.

Key Fundamentals of Private Label Development and Implementation

From my extensive experience in retail, I have learned that private label development serves three key purposes: strengthening branding, enhancing customer loyalty through unique products, and increasing profitability. Achieving these objectives relies on a meticulous step-by-step process, where each phase is critical. Missing even one step can compromise margins, affect targets, lead to flawed product development, and impact cost management efforts.

To attain success in private label development, attention must be given to several key aspects, from initial development to final implementation. These include:

Negotiating Costs: Start by focusing on fast-moving items. By leveraging high volumes, you can negotiate better deals and reduce costs effectively.

Defining Specifications: Ensure that your product specifications are clearly outlined and at par with the quality of national brands. This like-for-like comparison will build credibility in the market, demonstrating that your product meets top standards and that quality is never compromised.

Market Research: Take time to understand your competitors’ private label strategies and pricing. This insight will inform your own strategy and pricing decisions.

Sourcing Manufacturers: Evaluate both local and international manufacturers to secure competitive pricing without compromising on quality. It is crucial to balance high standards with cost efficiency to achieve success. Leading retailers often source their private labels globally to optimize both quality and cost.

Pricing Strategy: Ensure that the product’s cost price allows for a retail price difference of 15 to 20% compared to category leaders, along with an additional 15 to 20% margin. This principle has consistently guided me in scaling private labels effectively.

Contract Management: Establish contracts with manufacturers that cover volume requirements, pricing, lead times, product and packaging specifications, and penalty clauses for non-compliance. Regularly reviewing and adjusting these terms helps you stay agile and responsive to market changes.

Quality Control: Continuously monitor the quality of your private label products. Implement stringent quality control processes to uphold product standards. I recommend using a third party for random quality checks to ensure adherence to the agreed-upon standards with the manufacturer.

Brand Strategy: Deciding whether to use an existing brand name or create a new one significantly impacts your overall brand identity. Regardless of the choice, the brand will reflect the company’s value proposition and influence its reputation. Ensuring high-quality products is essential for strengthening brand identity.

Legal Compliance: Make sure you comply with all legal requirements and secure exclusivity for your brand name. This protects your brand and ensures regulatory compliance.

Packaging: Designing packaging that enhances the perceived quality of your product and meets legal standards is something I have learned to prioritize. Effective packaging can make a big difference.

Tiered Pricing: Develop private labels for various price segments – low, mid, and premium. Assign distinct brand names to each segment to appeal to different customer demographics. For the low and premium segments, creating specific brand names is especially effective.

In-Store Display: Allocate adequate shelf space for your private labels and position them at eye level. Proper placement can significantly boost visibility and sales.

Promotion: Plan regular promotions through catalogs, online channels, and social media. Utilize loyalty programs to encourage repeat purchases.

Price Monitoring: Regularly review and adjust prices to remain competitive. Periodically renegotiate costs with manufacturers to keep your pricing strategy effective.

Supplier Partnership: View your private label suppliers as partners. Regularly review their performance to address issues like quality and pricing, and use customer feedback to drive continuous improvement.

Fresh Food Quality: For fresh food and perishable items, maintaining consistent quality and safety is crucial. Your brand must be associated with reliable and high standards to avoid any perception of inconsistency or poor quality.

Supply Chain Management: Efficiently manage your supply chain to prevent disruptions. Streamline processes to ensure timely and reliable product availability.

Sales Monitoring: Regularly assess the sales performance of your private labels within their categories. Set targets for the next 3 to 5 years. For categories with limited or no brand presence, aim to achieve up to 75% sales contribution for your private label.

Customer Feedback: Collect feedback through surveys, focus groups, and blind testing to refine your products. Use this input to make improvements and better align with customer needs.

In summary, a well-executed private label strategy can greatly enhance a retailer’s brand, profitability, and customer loyalty. Achieving this requires a comprehensive approach that includes in-depth market research, strategic partnerships, innovative product development, effective marketing, and rigorous quality control.

In the current Philippine retail landscape, despite the presence of dominant international and strong local brands, strengthening private labels remains an opportunity for retailers to enhance their commercial offerings and reflect their company’s size and capability. Furthermore, a stronger market share in sales would significantly impact their economic model.

Reflecting on my early encounter with “white products” at Cora in the 70s, it is evident how far the concept of private labels has evolved. What started as a curiosity about cost-effective, unbranded merchandise has become a cornerstone of my strategic approach to private labels, helping retailers achieve success.

I hope these insights inspire you to fully embrace the potential of private labels in your own retail journey.

Postscript: For those looking to advance their private label strategy, consulting Philippe Devismes is highly recommended. As a mentor during the development of Aswaaq’s private labels, Philippe’s expertise and attention to detail offer invaluable guidance. His insights can help retailers effectively leverage private labels to enhance their market position and drive sustained success. Connect with Philippe on LinkedIn for more information.

A well-planned store layout can make or break your business. A thoughtfully designed layout not only enhances the shopping experience but also maximizes sales and improves customer satisfaction. Here are key reasons why planning your store layout is important and why standardizing it is essential.

Maximize Sales and profit

Anticipate customer flow management

Strategically plan the placement of the destination departments

Plan impulse buying

Enhance Customer experience

Ease navigation

Create a comfortable shopping environment

Plan the cash counter line to ensure efficient and friendly customer experience

Plan services

Optimize space

Maximize space allocation

Ensure efficient use of Aisles and displays

Plan category allocation

Enhance Marketing and branding

Anticipate thematic zones

Plan promotional displays

Improve Operational efficiency

Plan traffic flow according to customer behavioral patterns

Improve employee efficiency

Improve stock management and replenishment

Ensure safety and security

Design layout to minimize accident risks

Comply with local authority requirements and regulations

Prevent pilferage through strategic layout design

Why is it important to standardize your store layout?

Streamlined expansion

Clarify/Simplify site selection process

Replicate successful store model

Faster time to market

Cost-effective development

Achieve economy of scale in areas such as:

Store design

Construction and fit-out

Equipment and fixture procurement

Visual concept material

Maintenance

Process efficiency

Streamline the planning and implementation process of the stores

Reduce time and resources required for each new store

Standardize merchandizing principles

Space allocation per category

Category adjacency

Planogram

Vendor management

Facilitate uniform standard operating procedures

Eased data analytics

Easier data analysis and comparison from various stores

Stable foundation for predictive analytics model

Brand consistency

Ensure consistency across the different locations of the supermarket chain

Marketing and promotions

Facilitate the execution of marketing strategies and promotional campaigns across all stores

The retail industry is a narrative of two stories, each reflecting the dynamic interplay between consumers and business innovation. Together, these two halves paint a vivid picture of an industry in flux, where adaptation and innovation are paramount for success.

This report provides you with an indispensable tool to navigate and strategically position yourself amidst the dynamic shifts of the market. Inside, you will find news and articles from the first half of the year, insights into the consumers of 2024, and how the lines between online and offline retail experiences are blurring. It also explores how businesses are embracing digital transformation, reshaping their stores and supply chains to seamlessly integrate into this new retail paradigm. Additionally, it introduces you to the new players emerging in the retail market.

At RetailWise, we firmly believe that keeping a finger on the pulse of what the market wants isn’t just a strategy but the heartbeat of a successful business.

Below are the snapshots of what you will find in this report.

Retail News and Updates

National Players Update

Sustainability in Philippine Retail

Philippine Consumer 2024

The Future of Retail: What’s Ahead for H2 2024 and Beyond

Conclusion:

The insights gained from the first half of the year provide a crucial foundation for navigating the retail landscape in the second half and beyond. Understanding the trends, challenges, and consumer behaviors observed in the first half of the year equips retailers with strategic foresight. This knowledge allows them to anticipate market shifts, refine their strategies, and capitalize on emerging opportunities in the second half and beyond. By leveraging these insights, retailers can adapt more effectively, enhance their competitiveness, and drive sustainable growth in a dynamic and evolving retail environment.

Moreover, staying informed about retail trends in the coming months is crucial for understanding evolving consumer behaviors and preferences. By focusing on who today’s consumers are and anticipating the trends of tomorrow—such as increased digital engagement, sustainability concerns, and demand for personalized experiences—retailers can adapt proactively. Embracing innovations like AI-driven personalization, augmented reality shopping experiences, and eco-friendly initiatives will be key to capturing consumer interest and loyalty in the future retail landscape.

Stay updated with RetailWise’s comprehensive Retail Report for H1 2024! Gain insights into the latest developments and trends in the retail industry at global, regional, and local levels. Discover innovative advancements and understand the dynamic changes shaping the retail sector. Don’t miss out, click below to stay ahead in the retail world!

Out of the eight billion people in the world today, 64% use the internet, double the rate from a decade ago. Internet access has disrupted consumer life, including how they shop. Euromonitor International forecasts that consumers will spend nearly USD11 trillion on goods and services bought online in 2024.

This growing digital base needs to be at the center of your retail strategy. At NRF 2024: Retail’s Big Show in January, I spoke about the digital shopper trends that will have the biggest impact on retailers and brands. Let’s break down three big ones to watch in 2024.

Intuitive E-Commerce

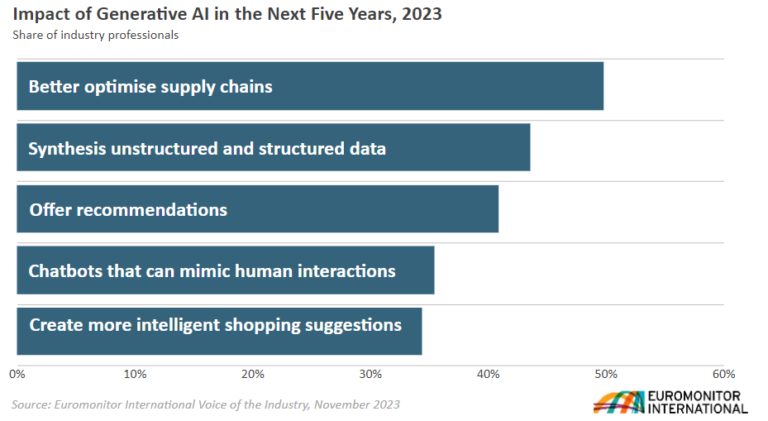

The rising influence of digital channels is putting pressure on companies to improve the online experience. This is becoming possible due to evolving data-gathering strategies and emerging technologies, from AR to IoT to generative AI. These advances have the potential to transform the online shopping experience, leading to one that is more intuitive.

Consumers have greater expectations. About half of digital consumers want one-of-a-kind offerings. A fifth note the desire for more personalized shopping experiences. In both cases, these sentiments are higher among the most digitally savvy population, according to Euromonitor’s consumer research. That is telling as this shift toward a more intuitive experience is playing out on digital channels where these consumers shop more frequently.

In part, this means ensuring the online channel is more akin to what a consumer might experience in person. While a variety of data and tech will be used, generative AI is poised to take on a central role in shaping the online experience. Generative AI can be leveraged in a variety of ways, from improving customer service to tailoring marketing messages to optimizing supply chains.

Virtual assistants powered by generative AI can create a more intuitive experience by using additional information sources for added context. Zalando’s new chatbot offers suggestions based on natural questions the shopper might ask, and in the future, could be combined with personal preferences, taking steps toward making the discovery experience feel more intuitive.

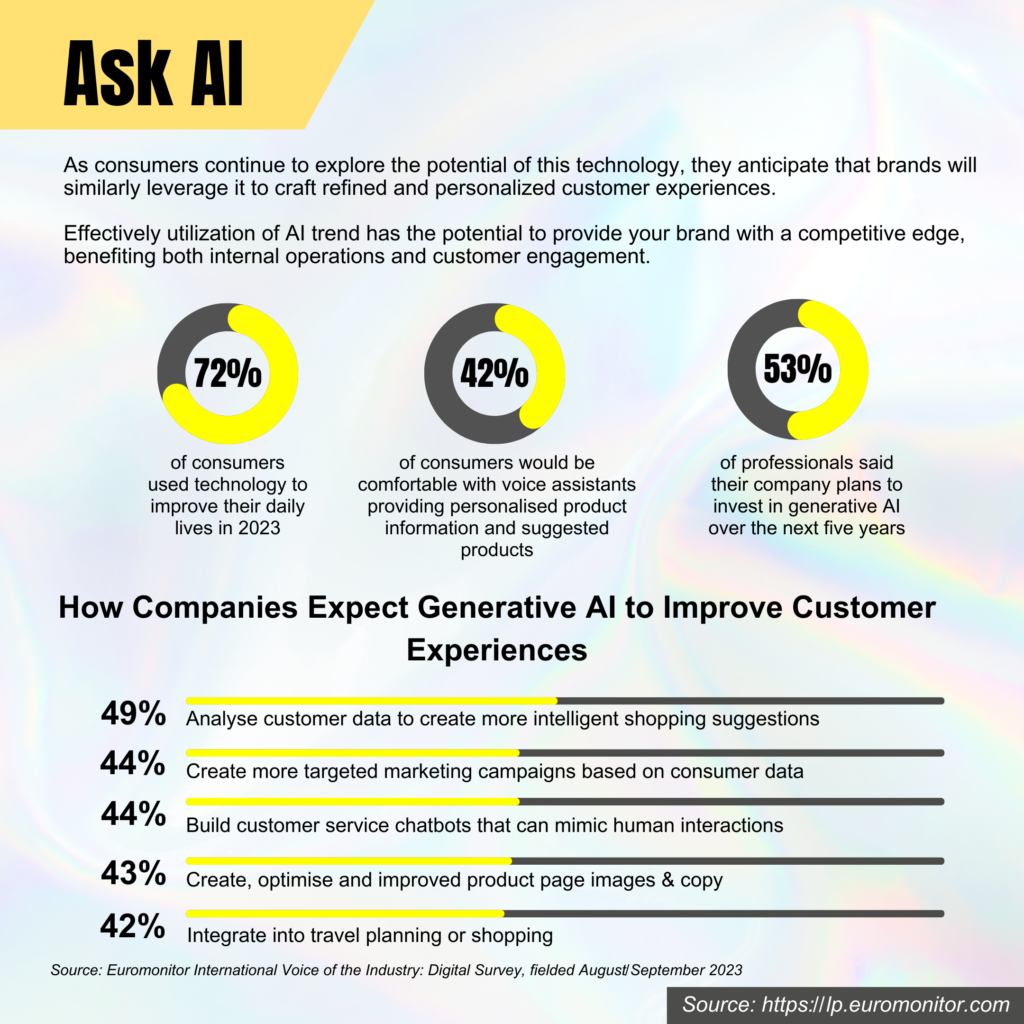

Almost half of industry professionals say they plan to invest in generative AI in the next five years

Source: Euromonitor’s Voice of the Industry Survey, 2023

New technologies like generative AI could give brands a competitive advantage. The pioneers who can create a next-generation shopping experience using these advances will be the ones that fuel a new shopping behavior and usher in the next so-called “Uber moment.”

TikTok Economy

Digital consumers are flocking to TikTok and its Chinese sister platform, Douyin. Brands are striving to promote their products and services on these platforms known for their short-form video content, but some of the viral trends that are doing the most to boost brand sales are emerging organically from users on those platforms.

These ByteDance platforms are not only some of the most popular, but also the fastest growing. As of 2023, 43% of digital consumers globally report using them monthly, a 19-percentage-point jump in three years, according to Euromonitor’s Voice of the Consumer: Digital Survey. These short-form video platforms, also known for their endless scroll and advanced algorithms, are a hit with young consumers, especially Gen Z.

Although most marketing campaigns on TikTok are financed or initiated by brands, some of the most viral content is organic. In 2023, an Israeli TikTok influencer posted a video of herself wrapping a frozen Betty Crocker Fruit Roll-Up processed snack around ice cream to create a crunchy fruit-flavored ice cream cone. Almost overnight, Fruit Roll-Ups began flying off shelves, creating a black market.

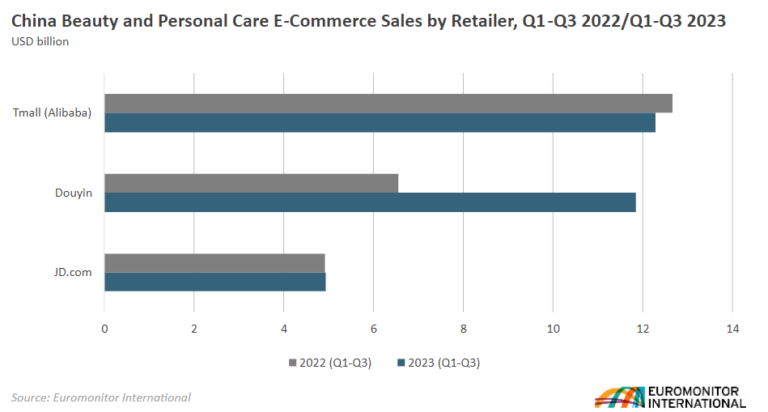

ByteDance platforms are dabbling in retail. In 2020, Douyin pivoted from being a pure social media platform to a retailer, prioritizing smaller sellers with a low-fee structure with revenue supplemented by advertising. Douyin has seen massive e-commerce gains. Online sales of beauty and personal care products on Douyin’s marketplace surged 81% in the first nine months of 2023, as compared with the same period in 2022, according to Euromonitor’s new e-commerce research. As for TikTok, its TikTok Shop is finding success in Southeast Asia and set up shop in the US and UK in September.

Revamped Returns

Consumers have long wanted hassle-free returns but delivering on that expectation has not been without challenges. The convergence of trends, like the rise of e-commerce, closure of stores by some retail chains and boost in sustainable strategies, is moving returns up the industry agenda. New technologies and partnerships are paving the way to a happier return experience for shoppers.

Creating a hassle-free return experience is not without challenges. First, what is deemed hassle-free varies by consumer. Although 43% of digital consumers point to mail as the preferred channel for online purchase returns, preferences vary by generation. For example, baby boomers prefer to return by mail, while Gen Z prefer to return in-store. To solve the unhappy return experience, the industry needs to shift its mindset, viewing this as being about improving loyalty, rather than a revenue drain.

Retailers are deploying a variety of tactics to reduce returns or at least their impact on the bottom line. Electronics specialist Best Buy is opening 10 smaller outlets, specializing in selling used and refurbished electronics. The aim of these stores is to target budget-conscious shoppers and recoup more from open-box and return products. More and more retailers are outsourcing the return experience to companies like Happy Returns or Loop Returns, which provide merchants with a customizable online portal for returns and exchanges.

To date, many retailers have struggled to grasp the pivotal role returns play in shaping customer loyalty and, as such, have sidelined this moment. That’s changing.

Two-thirds of retail professionals said they plan to continue or even accelerate investment in product returns

Source: Euromonitor International’s Voice of the Industry: Retail Survey

Looking ahead

These trends demonstrate how online shopping continues to mature, improving the customer experience from the moment of discovery to potential product return. A second, prominent theme is how consumers desire more power in their relationship with brands. TikTok Economy is rooted in how consumers are using social media to gain power in the value exchange. This power has led to more authentic messaging, which resonates with younger consumers like Gen Z.

As you begin to execute your 2024 strategy, use these insights to guide your campaigns, decisions and growth plans with the most digitally savvy consumers.