Global e-commerce spending will be led by millennials this year and they prefer online versus in-store when it comes to shopping.

Those are top findings from an ESW Global Voice survey that revealed more than 25% of millennials will spend more online this year when it comes to health, beauty, apparel, consumer electronics and luxury items.

The study also revealed nearly 73% of millennial shoppers plan to spend the same or more online in 2023, which will make this cohort the leader in global e-commerce spending this year, according to a press release on the findings..

“The millennial consumer remains fully committed to their preference for online shopping over physical retail,” Patrick Bousquet-Chavanne, president and CEO, ESW Americas, said in the release. “Millennials’ spending power has grown to $2.5 trillion, and they are not yet even in their prime earning years. They are spending more online than in-store across several categories, and these results indicate that brands must continue to evolve, improve, and optimize their e-commerce to attract and retain this increasingly powerful demographic.”

The survey’s polled more than 16,000 respondents across 16 countries comprised international shoppers across all demographics.

Additional findings include:

See the full report of ESW: https://esw.com/wp-content/uploads/2022/01/global_voices_2022.pdf

Sustainability in fashion is more than just a trend. Consumers demand it. Thanks to modern technology, shoppers now get more information about every piece they purchase with just a click. The consumers of tomorrow—Millennials and Gen Zs—want wearable items that support their causes, which pushed brands not just to make beautiful clothes and accessories, but something that has more substance in their style.

Proving how sustainability plays in Millennials and Gen Zs’ shopping is Zalora’s Southeast Asia Trender Report 2022. According to the lifestyle e-commerce platform, shoppers belonging to those age demographic “are prioritizing sustainability in their purchasing decisions.”

“Both Zalora’s Earth Edit and pre-loved segments saw substantial growth year-on-year,” the e-commerce platform states. “Total sales for Earth Edit, which focuses on the use of sustainable materials, increased by 152 percent from 2020 to 2021 and continued to have double-digit growth as of Q3 in 2022. Brands have reacted to this trend by expanding their product offerings on Zalora.”

Its pre-loved segment, although still very small, also saw a sharp growth of 70 percent from 2021 to 2022, led by Millennials and Gen Zs who will continue to drive the momentum for circular fashion, as per Zalora.

“As a push towards carbon-neutral continues to underscore fashion and e-commerce, brands can stand to gain market share by introducing more sustainable products while reviewing their supply chains,” Zalora added.

Its report also mentioned how Gen Zs spend most on sports-related products (29 percent), followed by apparel (25 percent). Both Millennials and Gen Zs lean more toward purchasing sports lifestyle shoes and sports performance shoes. Meanwhile, consumers of all ages are also adding to cart sports electronics, giving it a 15 percent growth from 2021 to 2022. Zalora concludes that this reflects consumers prioritizing health and wellness in our pandemic-new normal milieu.

“As for the biggest spenders of wellness products in Southeast Asia, Zalora’s data shows they come from Indonesia and the Philippines,” it says. “Across the region, adults above 40 spent the most, followed by Millennials aged 26 to 30.”

The Trender Report 2022 is based on a comprehensive analysis powered by Zalora’s retail intelligence and data analytics solution, Data by Global Fashion Group, to forecast consumer megatrends and purchasing patterns that will inform and shape retail strategies for 2023. It also includes intel from close to 60 million monthly visits, complemented by insights driven by Google and other partners.

“The nascent Southeast Asian e-commerce landscape is undergoing a significant digital transformation. Even as we brace for the potentially volatile climate ahead, it has become increasingly important for brands and retailers to connect with consumers in the right way,” said Gunjan Soni, Zalora Group’s chief executive officer. “Our flagship state-of-the-industry report helps to guide the industry through this unpredictable time and aid in their retail strategies as they navigate through the region’s diversity and build on the momentum.”

To know more about Zalora’s Southeast Asia Trender Report 2022, click here.

Throughout history, the use of technology has had a significant impact on improving people’s way of life. Humans have been successful in transforming these technologies into innovations – examples are products that promote better health and lifestyle, and processes and services that streamline how we work and how we do things. But the real measure of the impact of any technological innovation will depend on how far we reach out to others. In other words, innovations should not choose demographics, education, age, or income class.

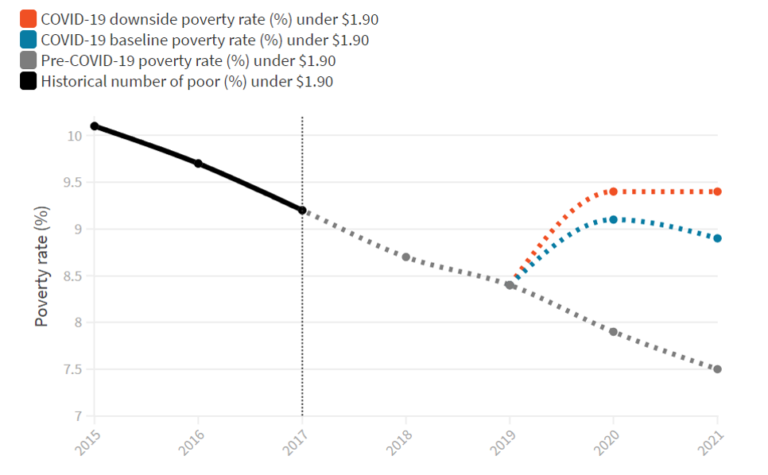

In “The Fortune at the Bottom of the Pyramid” (2007), C. K. Prahalad shared a radical idea combined with substantial research data on alleviating poverty through economic development and social transformation. According to Pralahad, there is an estimated four to five billion people within the global population living with less than USD 2 a day who are at the Bottom of the Pyramid (BOP). Recent data from the World Bank shows that in 2017, an estimated 9.2% of the global population of approximately 689 million people lived in extreme poverty. Last year, the COVID 19 pandemic has increased this number by an estimated 88 – 115 million people (measured through the International Poverty Line of $ 1.90 /day).

Figure 1: The impact of COVID-19 on global extreme poverty

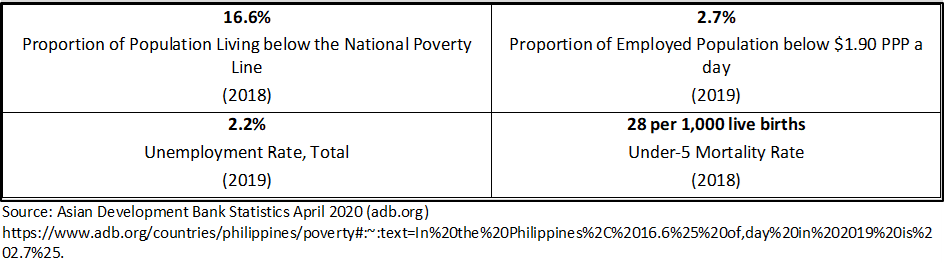

According to studies conducted by Asian Development Bank in 2018, in the Philippines alone, 16.6% of the country’s population, or approximately 17.6 million Filipinos lived below the national poverty line. Additionally, the 2019 data shows that the percentage of the employed population living below $1.90 PPP (purchasing power parity) per day is 2.7%.

Figure 2: Poverty Indicators (Source: Asian Development Bank Statistics April 2020 (adb.org)

This consumer group remains unserved by large businesses possibly due to the lack of strategies on how to reach out to this unique niche market segment or businesses are simply not aware of their potential engagement and loyalty.

Awareness and recognition of the bottom of the economic pyramid and eventually the development of products, processes, and services catering to the “poor” group can potentially lead the way to a new approach in looking at a profitable business. Companies will need a fresh set of eyes and mind to be able to come up with ideas on how they can support this underserved and mostly unbanked population which will impact their lives and for the business to profit in the end.

To help businesses, here are important points of Prahalad’s Twelve Principles of Innovation for the Bottom of the Pyramid which can be used as a guide in creating or investing in technologies for their companies.

Focus on price performance. BOP consumers are looking for products that are affordable and yet come in the full package. With their limited budget, companies should create products and services that are not necessarily cheap but should be value for money with competitive pricing.

Innovate by providing hybrid solutions while blending old and new technology. BOP consumers prefer simplified, useful, and user-friendly innovations. Companies should think of how to transform existing technologies that would meet this market’s needs.

Make it scalable and transportable. In order to reduce cost and maximize sales through high volume, companies should develop products that would cater to the BOP consumers across cultures and languages as well as integrate economies to capitalize and market their products and services across distance and beyond borders.

Reduced resource intensity: eco-friendly products. As BOP Market needs to conserve their resources, companies should find better solutions to come up with products and services encouraging recycling, reduction of waste to create an eco-friendly environment.

Product Design with Functionality from the beginning. The BOP Market would look into practical designs of products and services that would meet their specific needs. Companies should be able to incorporate functionality but also be clear on how their technology will be used by their consumers.

Building process innovations. Standardization of processes combined with proper training can streamline and enhance a better business environment. This in turn can cut down costs and drive additional savings which can be passed on to BOP consumers.

Deskill (services) work. With the application of technology, automation will remove manual tasks and labor-intensive works can be mechanized, automated, and computerized. This could increase output significantly and provide cheaper products. Or companies can invest in technologies that would require fewer skills, therefore, simplifying the process.

Educate customers in product usage. Companies should be able to devise plans and strategies in how to teach their BOP market to be early users to be able to accelerate adoption through customer engagement and tapping influencers.

The product must work in a hostile environment. The environment where the BOP market is different so the overall package of a product should be considered as less sophisticated and should withstand noise, dust, unsanitary conditions, abuse, electric blackouts, and water pollution. Companies should be able to test their products for durability and expiration. Another important factor is making sure that customer support is available.

Simplified and adaptable user interface. Technological applications should be diversified and should be developed by companies to cover a wide consumer base. This will encourage user-friendly products which can lead to higher customer retention.

Innovate in Distribution. Companies should invest in technologies that can improve their procurement, distribution, and logistics in different environments such as dispersed rural markets or highly populated urban markets.

Focus on broad architecture to enable quick and easy incorporation of new features. Future add-on features which are added values to the consumers should be considered when investing in technologies and companies need to ensure that these features are easy to incorporate later on.

As companies use Prahalad’s 12 Principles to guide them in developing or investing in products and services, it is also critical for them to ensure that BOP is present in space. In the Philippines, more than half of the total population as of January 2020 were internet users (statista.com). But according to Bangko Sentral ng Pilipinas latest financial inclusion survey, there is still a wide gap in digital literacy between income brackets. Only 40% of Class E are digitally literate. As companies diversify from offline to online, they can leverage by creating awareness programs and campaigns to transform the BOP into a solid digital market. Converting them as digital consumers is a crucial step in adoption and will therefore play a vital role in any company’s success.

Awareness and recognition of the bottom of the economic pyramid and eventually the development of products, processes, and services catering to the “poor” group can potentially lead the way to a new approach in looking at a profitable business. Companies will need a fresh set of eyes and mind to be able to come up with ideas on how they can support this underserved and mostly unbanked population which will impact their lives and for the business to profit in the end.

With the massive adoption of mobile technology, companies should create strategies to include the Bottom of the Pyramid in their target customers. This population should be viewed as an important, growing, as well as a viable, and profitable market. The BOPs can afford to buy unique, low cost but good quality and sustainable products and services mostly in cash and can be potential loyal customers. And as we move further to a more digital economy, companies can benefit from paying attention and supporting the needs of the Bottom of the Pyramid by incorporating.

Enhanced Instacart Pickup service now live at 1,500 supermarkets in 30 states Instacart is doubling down on click-and-collect online grocery service with an upgraded Instacart Pickup product and a nationwide rollout to retailers by the year’s end.

To support the expanded grocery pickup business, San Francisco-based Instacart on Tuesday named company veteran Sarah Mastrorocco as general manager of Instacart Pickup, a newly created position.

Currently, Instacart Pickup is available at more than 1,500 stores in 30 states through over 50 grocery retailers, including Albertsons, Publix Super Markets, Wegmans Food Markets, Schnucks Market, Price Chopper, Gelson’s Markets, Shop ‘n Save and The Fresh Market. Plans call for the service to be live at supermarkets in all 50 states by the end of 2020, Instacart said.

“2020 is the year of pickup. For our retail partners, we’ve seen Instacart Pickup become a gateway to growth in a margin-thin industry,” Instacart President Nilam Ganenthiran said in a statement. “Our pickup product is also becoming a significant revenue contributor for our retail partners, growing customer basket size by an average of 15% and accounting for an average of 20% of a retailer’s total Instacart store sales.”

Instacart said its “reimagined” pickup product has launched gradually at grocery retailers in recent months and is now available across the United States and Canada. Among the key new features is Smart Storefronts, which enables customers to view

delivery and pickup options from one digital storefront for each of the grocers they shop on the Instacart platform. As a result, users can now toggle between delivery and pickup options to see the latest inventory by store and compare time windows for both.

The updated Instacart Pickup also facilitates collecting after clicking. Pick Your Pickup Mapping functionality allows customers to view and choose the pickup location most convenient to their route that day, such as when coming from home, work, soccer

practice and elsewhere. In addition, customers can now enable location-based notifications, known as On The Way Alerts, to let their store know when they’re on the way and getting close. That allows in-store shoppers to be ready and waiting for

Gelson’s has expanded its partnership with Instacart to add pickup to all of its store locations.

“At Gelson’s, Instacart Pickup is an integral part of the way we’re evolving to meet the changing needs of our customers, who appreciate the flexibility and affordability that comes with a curbside offering. We recently expanded our partnership with Instacart to add pickup, in addition to delivery, across 100% of our store locations,” said John Bagan, chief merchandising officer at Encino, Calif.-based Gelson’s Markets. “With this new partnership, customers can now have groceries and household essentials as well as beer, wine and spirits ready for same-day pickup. While still early days, Instacart Pickup is growing double-digits for us quarter over quarter, making it clear how much our customers value — and have come to rely on — this new experience.”

Other new Instacart Pickup features include customized navigation, which sends customers to the mapping app of their choice to automatically direct drivers from their current location to the store. Users, too, can now share their order details with friends

and family to designate another driver for an order pickup. Instacart added that it’s also continuing to expand alcohol pickup service, currently offered via 20-plus retail partners, including Aldi, BevMo!, Publix, Save Mart, Sprouts Farmers Market and Wegmans.

“We first partnered with Instacart to bring Cub stores online with delivery in 2015 and, based on the overwhelmingly positive customer response, last year we expanded ourInstacart partnership to include pickup across nearly 100% of the Cub store footprint,” according to Darren Caudill, senior vice president of sales, merchandising and marketing at Minneapolis-based Cub Foods. “Cub Foods customers are shopping online more than ever before, and having a seamless pickup experience is an important part of the digital offering we’re building for those loyal customers. It’s also been a boon for our business. We’ve seen our pickup business double in the last three months alone.”

Instacart said it’s launching pickup service at hundreds of stores monthly and expects to more than double the number of locations offering the service this year.

“Instacart’s broader business continues to grow at an incredible clip, with pickup as our fastest-growing product,” noted Ganenthiran. “With the completed rollout of the new Instacart Pickup and the appointment of Sarah as our new GM, we’re laying the groundwork now to prepare for another year of triple-digit growth. By year-end, we expect to have the largest pickup retail footprint in North America and, in the coming years, to grow Instacart Pickup into a multibillion-dollar business.”

In her new role, Mastrorocco (left) will work with partners across the Instacart organization to oversee and scale the fast-growing pickup operation, the company said. She joined Instacart nearly six years ago as the first member of the business

development team and then served in various leadership posts in such areas as catalog and account management. Most recently, she was vice president of business development. Before coming to Instacart, Mastrorocco was a member of PepsiCo’s

Global Operations Group, working on direct-store delivery operations in North and South America, and served on Frito-Lay North America’s strategy and M&A team.

“As we’ve come to understand the massive growth opportunity ahead for this product, it made sense to deepen our commitment to Instacart Pickup and grow our team to prepare for a year of expansion and innovation in the space,” Mastrorocco told

Supermarket News. “I’m thrilled to have the opportunity to lead this work — which is powered by a very talented group of people, including product managers, machine learning engineers, data scientists and operations researchers — to better serve the pickup business and deliver more innovative products for customers.”

Instacart Pickup debuted at a handful of retail partners in 2018, and last year Instacart doubled the number of retailers and tripled the number of states offering the service. Mastrorocco reported that pickup accounts for 20% of a store’s overall Instacart sales within four to eight weeks of the service’s launch.

“Today, we have more than 350 grocery and retail partners on our marketplace, and more than 50 of those now offer pickup as an option. That’s a lot of green pasture to power pickup for our industry,” she said.

For consumers, online grocery pickup is a natural evolution from home delivery, Mastrorocco added. “The growth we’re seeing is rooted in what we’re hearing from our customers. Consumers are in the driver’s seat more so than ever, and pickup gives

them one more highly flexible and affordable option to choose from,” she said. “Whether they’re doing their weekly shop, stocking up with pantry essentials, or shopping for a special recipe, people love being able to choose how to get what they want.”

On the delivery side, Instacart’s service is available at nearly 25,000 stores in more than 5,500 cities in the U.S. and Canada, serving over 85% of households in the U.S. and more than 70% of households in Canada.

Read original article: https://www.supermarketnews.com/online-retail/instacart-sees-2020-year-grocery-pickup

It is not a secret to everyone that the key to getting as many customers as possible is understanding everyone’s constant quest for convenience. This goes to say that a retailer’s main priority is to make sure that the business is accessible to every consumer at any given point of time and that the transactions are not just easy but fast. But more than the demand for convenience, some consumers are also doing their part to assure the efficiency in their transactions. Moreover, collective consideration and shared responsibility among consumers show a promise of faster retail and further convenience for everyone.

Japan had been known worldwide as a country offering convenience and efficiency. Through innovative business solutions, big or small, Japan is becoming more and more a benchmark for every retail market in the world. Customer service is the language of every retailer. Japanese consumers are also known to be one of the most unforgiving in this aspect. In a survey conducted by American Express International, 57% of Japanese respondents answered that they immediately stopped or never went back to an establishment after just one bad incident. Since Japanese consumers are willing spenders, one customer lost already means bad business.

Though convenience can be seen in every nook and cranny of Japanese retail, Japanese culture also suggests a shared responsibility and consideration towards everyone. In this regard, a person new in Japan can notice even the smallest practices that Japanese normally observe.

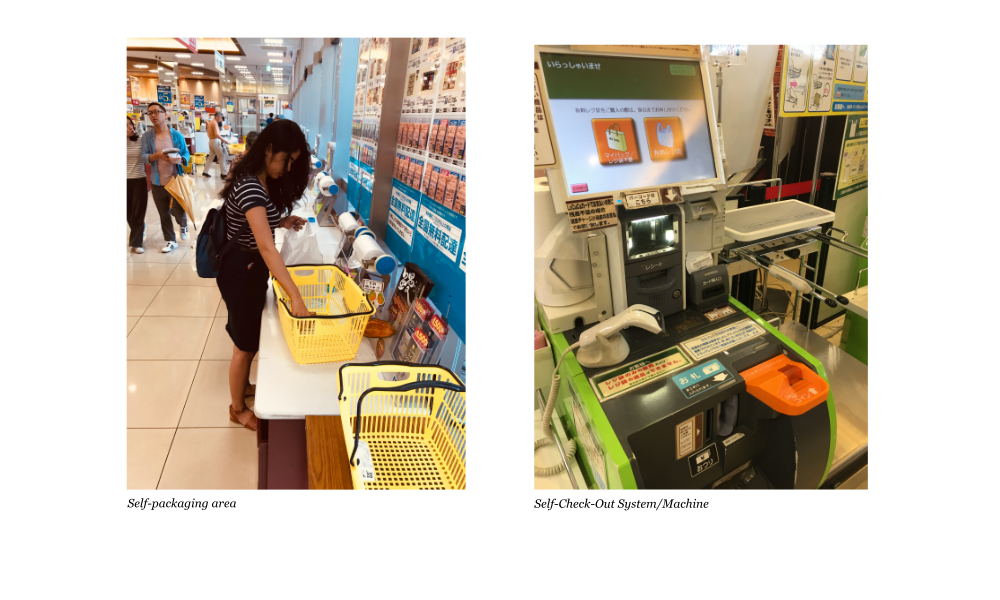

For one, most restaurants practice the “claygo” method or clean-as-you-go. Every customer is obliged to clean up their own tables after using it and take their trays and used utensils in a designated counter. This doesn’t only help the staff by reducing their work, but this also lessens the waiting time to be seated in a vacant table as it’s ready for use once the customer stands up. Additionally, it is also considered normal for every supermarket to have its area designated for packaging as customers are also obliged to do it by themselves. More so, there are self-check-out counters where customers can scan, pay, and pack their own purchases. These are some of the reasons why you will almost never fall on queue in every supermarket as transactions are fast and efficient.

On a rainy season, you will normally see plastic dispensers outside establishments encouraging everyone to cover their wet umbrellas to avoid it dripping inside. This will not only give the staff less mess to clean, but this will also help avoid any accidents due to slippery floor. A trash bin is also available outside to assure the proper disposal and recycling of these plastics. This is considered a very simple practice but it has considerably good benefits both on the business and the consumers.

Recently, hotels in Tokyo are equipping themselves with unmanned reception counters where guests can check-in and check-out by themselves. Machines have cash slots and change dispensers as well as POS terminals to accept card payments. It is also complete with passport scanners to record details of the guest. Once all check-in procedures are done, the guest can choose between a card or pin code to get access to their respective rooms. Check-out, on the other hand, is done in very few steps and no checking of rooms is required before doing so. The trust that business establishments are placing on their clients is also being reflected by the honesty that is embedded deeply in Japanese culture.

Most people who went to Japan will talk about the level of convenience that every store or restaurant gives its people. Albeit, the level of responsibility that people also practice is another notable factor than can be attributed to Japanese culture. This is probably unique in Japan but foreigners who were not exposed to this culture had no difficulty in adjusting and doing it as well; they even found the benefits in doing so. Though obviously a factor, cultural differences will not be an enormous hindrance for other countries to start on these practices too. Convenience is definitely the language of retail but educating consumers is another angle that retailers need to look into to make a more beneficial, more convenient, and more efficient relationship with its consumers.

I would like to take the opportunity of this writing to wish you a very good 2019.

I am sure that the economic trend and lessons taken from the previous year about managing inflation will be favorable factors to the success of your plans and different ventures.

I had the opportunity to travel to France during the holidays. During my stay, I visited a lot of supermarkets and hypermarkets, two favorite French retail formats.

We have been hearing a lot of news about the degradation of the French economy and the action and impact of the gilets jaunes on the business during year end. This is probably true but I also saw a lot of customers in the stores buying profusely for the celebrations period.

I was impressed by the volume of merchandise available, the quality of the displays and the modernity of the concepts. Stores are not driven by a real estate approach, selling space to suppliers. You hardly find a brand signage, it is very clear that the store belongs to the retailer.

The goal which is selling more and more items to more and more customers is extremely felt in the outlets. The economic model is mainly based on volume sold. Quantity on display is not questioned and the depth of the range is not compromised, proposing a wide selection of regional products. Promotional displays for every end cap are massive with a large yellow signage, very often hand written. Dedicated discounts for loyal customers are available for each category.

Fresh displays are also impressive through volume, range, display quality as well as freshness of the products that transpires everywhere in the area. Stores are obviously equipped to maintain the cold chain. Street market ambiance is being preserved. We commonly say that we buy with our eyes, this will be held particularly true in the Fish, Delicatessen and Cheese sections. Similarly, you can hardly resist to the smell of the bread and “viennoiseries” section. You will also be amazed by the wide offering of pre-packed fresh food, so convenient for every family size.

Services proposed by retailers are convenience oriented. The “drive” concept (your order and pick goods) is largely developed. Customers are also now used to self-scanning options. Electronic labels are on every shelf, guaranteeing price accuracy.

We could argue that the French food culture is unique, the climate very favorable to Freshness, the hypermarket concept that started in 1960 is already mature: these are all true.

However I see this concept as an opportunity for inspiration in many ways. It starts with the principle of the concept: complete control approach by the retailer instead of being real estate oriented or vendor oriented, risk taken on the stock and promotions, commitment to promote regional sourcing, creating a sense of authenticity for the customers, specifically but not limited to the fresh sections. True and large benefits granted to loyalty card holders.

Advanced technology is only brought to enhance the customer’s shopping experience. Most of the solutions for faster payment are based on trust. Are retailers ready to give it to customers? Should the focus be on the process to progressively educate the customers?

With the online business development, physical stores are actually challenged. There is a trend to reduce big boxes assuming that a part of the business is and will be taken online. Convenience stores or smaller grocery formats are also seen as a threat. But in reality, they catapulted to growth as they occupied the space not covered by larger formats.

In fact, I see the size concern differently for the food retail business, particularly in countries wherein the size has been commonly compromised. Based on my experience, larger size stores with well-chosen locations provide retailers the opportunity to entirely express their commercial concept, and most often become the flagship(s) of the retail chain with a very superior sales level and an enviable profitability over time.

This might be perceived as counter trend but the “applicability” of the trend is a question of maturity in the retail business. Let us take this new year as a chance to seize the true opportunities awaiting us in the retail industry!

Majid Al Futtaim is famously known in Middle East as a retail company giant. Yet for people well-conversed in the retail world, Majid Al Futtaim is a business magnate who knows how to seize opportunities that is hidden from plain eyesight for most people. He is someone who knows how to set his vision and can dauntlessly invest time, resources and effort to make that vision a reality even on the long run.

1994 witnessed the opening of the first MAF Mall with Continent, one of the leading French Hypermarket brands, a main anchor tenant.

The hypermarket was built inside what is famously known today as Deira City Center. As of today, DCC is surrounded by commercial and residential buildings – a stark contrast to how it was 23 years before when it is situated in the middle of nowhere. Majid All Futtaim, through his vision saw this as a good opportunity. After all, why build a business surrounding others when you can let others surround yours?

Just as many success stories, Majid Al Futtaim faced difficulties particularly at the onset of his retail business. But the visionary know that stopping is not an option when it gets difficult. To make up for a better planning and management of the business, Majid Al Futtaim hired retail experts from Europe, mainly from France to help the business grow. Being a wise risk-taker, Mr. Majid knew that the key to make his business grow is investing on people who have the expertise and experience to prepare his business for development and to harness its potential for growth at its fullest extent, using the best retail standards and practices not just in France, but from the whole world.

And just as expected, the business grew. In 1998, MAF retail launched its second hypermarket branch in Ajman to spread its influence and exposure.

Majid Al Futtaim continued the vision to hold dominion over the region. Several branches quickly opened up in UAE particularly in Al Ain, RAK, Abu Dhabi and Sharjah. By year 2000, Carrefour’s acquisition of Continent enabled the change in the name of hypermarket’s name and logo yet the quality of services was not altered and still operated with the same recipe for its success: strategic sites, large footprint, mid to large size malls and strong hypermarket concept as a foot traffic driver. Furthermore, the change of the brand to Carrefour only strengthened with the support of French Retail Leader.

The peak of MAF’s success could be seen upon the development of Mall of Emirates. Being the visionary that he is, he built the mall despite its isolation and opened it in 2005. The mall is notable for its architectural design, innovation, accessibility, tenant mix, hotel selection and large hypermarket. Mall of Emirates is manifestation of group expertise in planning, designing, managing projects and operating malls. It clearly reflects the demand for perfection by its owner, Majid Al Futtaim. Easily, Mall of Emirates can be compared to top malls around the world.

The concept of “everything under the same roof” rapidly gained success. Year after year, it was improved and modernized while adding value to the product range. However, apparel department with basic items and poor development in novelty or fashion items remained its weakness. Similarly, Asian food product range used to be behind – a mistake considering that more than 50% of the population living in Dubai are Asians.

On a positive note, the management kept on modernizing the electronics and appliances department that hit the highest market share among Carrefour Stores worldwide. All thanks to the tax free environment in Dubai, which led to comparatively cheap prices attracting more visitors in the country. It is common to see people at the airport bringing home electronic gadgets that they had just purchased.

The management of the Fresh Department was also ameliorated step by step. The concepts such as bread and pastry, meat, and fruits and vegetables were improved to meet European standards.

The overall concept went through changes year after year, CEO after CEO. Moving from a basic supermarket to a modernized version of the hypermarket. The discipline in managing the stores was also a contributing factor – from asset standards to cleanliness, hygiene standards and product availability.

The competition surrounding MAF stores became progressively more aggressive each passing year. More retail brands opened, developed and benefitted from the positive economy of the region. Lulu, Carrefour’s main competitor, was able to develop faster with an arguably more flexible size and less complex concept than MAF Carrefour.

On the other hand, small and local cooperatives with scheme dedicated to national citizens and with comparatively cheap prices remain an alternative for the mass market.

Another brand, Spinneys, captures mainly the expats’ market with a more premium concept covering small and medium size supermarkets. Instead of fully competing with Carrefour, they went with a different concept, capitalizing on the superb management of fresh products as well as offering unique and exclusive imported product range. When it comes to the Asian products range however, Carrefour had also set its eyes to observe Choitram, particularly its supermarket concept.

Though MAF Carrefour was proven to be a true success in UAE, Oman and Qatar, its development out of its comfort zone had been sometimes challenged for various reasons.

It has always been said that there is no definite secret to success. Different stories, different recipes. Yet for Majid Al Futtaim, it is a story of setting the right vision and taking risks to transform it into reality. He followed his exemplary intuition then transformed them to opportunities. More importantly, he placed his trust on the people he surrounded himself with. He knew that these experts in the retail field will not fail him and the business they worked so hard to achieve. His business is not simply made of investments, it is made by people and for the people.

MAF’s group of advisers are always on the look for opportunities and propose strategic development. The relationship between Mr. Majid and his advisers can always be described as mutual friendship and protection. A solid partnership between parties that will not let each other down is one of the foundation of his business. However, knowing that change is constant, he doesn’t hesitate to change plans or people as the situation requires it. In this way, the company, despite being susceptible to change is always able to keep up and thrive.

Mr. Majid also knows that his company alone cannot be independent of government. He established a politically correct and good relation with Dubai Government, particularly with Sheik Maktoum. Sharing the same vision for development and success, MAF Retail had always been in close and cooperating ties with its “mother” government.

MAF Malls are not only a reference in the gulf region, but also a model for the retail industry worldwide. The expertise in developing and managing medium to large size malls and the transition of mass market oriented malls to reasonably luxurious malls were established. Mall of Emirates had always been considered as a piece of art in the industry offering innovations in entertainment such as ski station among others.

The tenant mix in the mall was improved and the attractiveness of the malls was also proven. Because of this, regional and international brands lined up to be part of MAF Malls despite considerably higher price for rent. The selection of restaurants was also well sought, from quick food to fine dining experiences.

Again, experts from other countries contributed to the growing success of the Mall concept, offering competitive advantage to Carrefour Hypermarkets.

From the opening of Continent in 1994 until early 2000’s, the head office structure was almost non-existent, limited to a CEO, a Vice President and CFO to ensure financial reporting. The management of the operations and the merchandise were totally delegated to the stores. But after 8 years of experience and maturity in the retail world, MAF Retail set a head office structure with a merchandising department.

Between 2003 and 2010, MAF Carrefour strengthened the corporate office and support to stores primarily due to the influence and help of a new CEO back then. With the expansion, an international head office was also created to ensure consistency in management across different countries, alignment in standards and correct setting of corporate governance principles.

Initially led by French Retail Experts from the support group to operations, the Profile of the managers progressively changed with a strong “Arabization” of the management which seemed to be a natural characteristic among Arab countries. Internal promotions were also prioritized to face the fast development pace.

As MAF Company evolved and grew in size, the corporate governance was put in place and control over MAF retail operations from the holding limited its autonomy, different from what the retail management enjoyed for several years. For the past decade, the management of the stores was totally strategized and controlled from the head office, leaving little space for individual initiatives. Thus, the influence of international experts is limited to core support functions of the head office as few remained to operations.

In 2013, MAF Holding acquired the remaining 25% stake from French Retailer Carrefour Group for 530 million euros. From a joint venture, MAF Holding held the regional franchise for Carrefour – the world’s second biggest retailer after Walmart. Under the signed agreement, MAF will own 100% of the shares and the franchise will be extended until 2025.

MAF continues to do excellently in its home country, UAE. 2017 was another year of record, however, there are some fears on the impact of the VAT implementation in the country after years of enjoying tax-free privilege.

MAF also continues to thrive well outside UAE as it is now present in 15 countries operating a total of 90 hypermarkets and 120 supermarkets.

Among the countries it had reached, Iran seemed to be a very promising country as one of the two Carrefour stores is already challenging the food sales performance of MAF’s branch in MOE. Pakistan also displays a promising market. However, Eastern European countries seem to be in resistance to the company’s proven model as it remains challenging to MAF Retail.

Mr. Majid is without any question the man who turned his vision into reality. The idea and process of developing medium to large malls with unique standards associated to a traffic generator such as Carrefour or Continent at the beginning was a very innovative strategy 20 years back in UAE and Gulf Region. It had not been an easy start and the risks are high, but the true visionary that he is, he decided to move forward. Fast forward to 25 years after his company was first founded in 1992, the success of Mr. Majid is nothing short of amazing.

In managing his business, Mr. Majid was able to avoid the traps of changing category, from a small company to a large company, he made it a point that strict compliance with corporate governance principles will remain. Another reason for its success can be attributed to the establishment of a proper delegation of authorities. While most business owners would have difficulties to let go of their businesses and delegate authority to the management in place, Mr. Majid put his trust on his people and did not waste time doubting the people who also put their trust on him. Delegations with proper control level have been in place since the beginning to the point that even Mr. Majid and his advisors have limited interferences in the day to day business as he had always put his focus on prioritizing strategic development for longer term goals in order to safeguard his company from possible challenges that could affect it in the future.

From this point, it will be needless to say that MAF Retail’s future is already envisioned somewhere in Mr. Majid’s mind. His actions are always determined by his plans and he’s someone who can hardly be caught off-guard by any incident or circumstance that will be brought to the retail world – which is how retailers must always strive to be!

As most countries in Asia, Indonesia’s retail also relied on traditional-oriented market. However, in the recent years, Indonesia had a visible growth in modern retailing. The growth and trend in modern retailing was fueled by the rising middle class, higher consumer confidence, rising personal income and with the majority of its population being more conscious and inclined to imported brands.

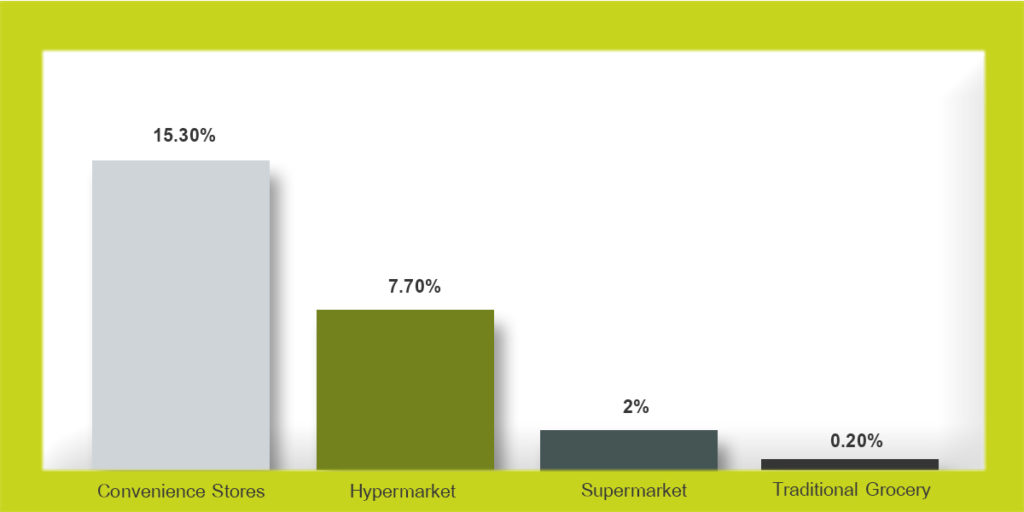

Traditional markets still continue to dominate the retail sales at 83.25% and modern retailing accounting for the other 16.25% (supermarkets, hypermarkets and convenience stores) on 2015 according to the latest data by Euronomonitor. However, growth on the number of outlets for traditional market is comparatively low to the growth posed by modern retailing outlets. The growth in traditional market by 2015 accounted only to .2% while the modern retail channels had significant growth – supermarkets at 2%, hypermarkets at 7.70%, and convenience stores at 15.3% also on the same year.

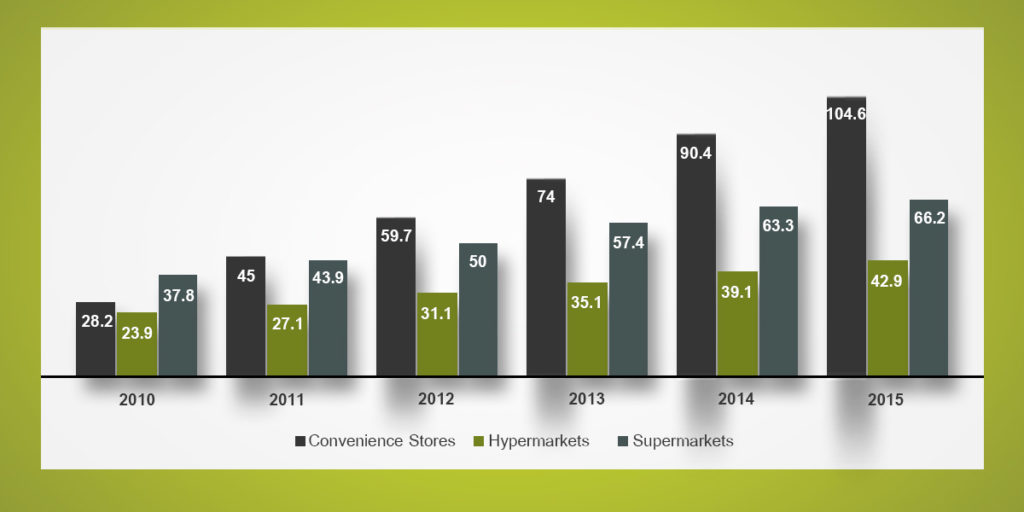

Convenience Stores hold the largest sales among modern retailers accounting to 104.6 trillion IDR followed by Supermarkets with 66.2 trillion IDR and Hypermarkets with 42.9 trillion IDR, all in 2015.The three store formats posed continuous growth within the past years indicating that modern retail in Indonesia is a trend accepted more and more every year.

Though traditional markets had been the center of retail activities in Indonesia for years, big malls, supermarkets and convenience stores are quick to replace this retail channel as they show convenience as well as entertainment.

Expansion of Indonesia’s modern retail started in 1999 when the government allowed Carrefour, a French retailer to expand its operations in the country. As of today, the company is locally owned and operated by Trans Retail under the name of Trans Mart with 92 branches nationwide. More modern retailers from different countries followed and made their entry in Indonesia – Lotte Mart from South Korea which has now 43 outlets, Hero from Hong Kong which has now 35 outlets and the latest entry is on 2015 with Aeon Supermarket from Japan. Local major retailers still prevail in the retail landscape. Most notable among the local major retailers are Alfa Midi with 1,022 outlets, Giant with 172 outlets, Lion Superindo with 136 outlets and Hypermart with 112 outlets. Some of the companies operate various store formats: hypermarkets, super markets and mini groceries.

Convenience Store are expanding rapidly in Indonesia every year. The introduction of 7/11 in 2009 paved way for more outlets to expand throughout the country. Indomaret is a local convenience store holding the most number of outlets nationwide. As of today, Indomaret operates13,099 stores. This is followed by Alfamart with 11,115 stores and the rapidly expanding Circle K which has now 500+ stores.

Supermarkets and convenience stores did not only grow but also developed. Top supermarket retailers have wide assortments of imported products that are readily available for locals and foreigners in Indonesia. One of the primary reason why foreign nationals won’t find it hard to shop in the country.

Besides the wide assortment, both local and imported products, supermarkets and hypermarkets also have in-house bakery and a food-to-go section, making every shopper’s need available in one roof.

As stated in the data above, convenience store shows the largest growth among all the retail channels in the country. Approximately, there are 25,278 convenience store/minimarket outlets constituting to a 15.3% growth rate on the number of outlets in Indonesia (Euromonitor, 2015). The growth of convenience stores is a trend observed in other Asian countries as well. In the Philippines for example, the growth rate in convenience store outlets is at 20%. However, the real store count falls far behind compared to that of Indonesia as it only has approximately 3,687 outlets according to the same source. The success of convenience stores in Indonesia could be attributed to the fact that there’s a higher population density among its major cities, notably in Jakarta. Higher population density poses higher demand for convenience as most people would prefer to shop on mini groceries or convenience stores in every street corner than spend more time in the usual traffic jam and extra budget to pay for fare going to supermarkets or shopping centers.

Moreover, it is also worth noting that convenience store channel in Indonesia doesn’t only increase in number but also innovate. More than just a place where people can complete their basic purchases, a standard convenience store in Indonesia also serves as a place where people can transact different services such as bills payment and money remittance center. Their convenience stores are also equipped with ATM Machines inside where people can easily withdraw cash from their cards. Taking a “one-stop-shop” to a new level, most stores have wider dining areas where a free wifi can be accessed.

Promising potential in Indonesia’s E-Commerce

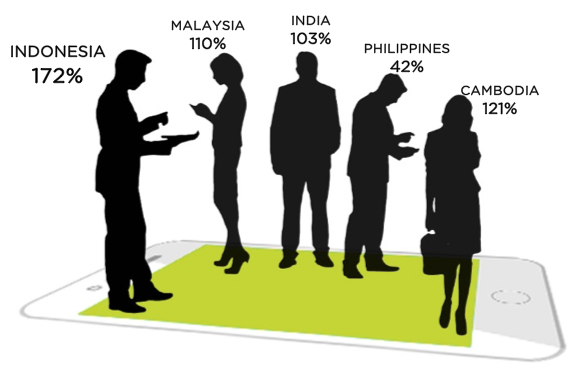

E-Commerce also has a very promising potential in Indonesia as it is the country with the most mobile internet subscription among its neighboring Asian countries. It has a 172% growth rate far from 121% of Cambodia. Philippines falls far behind at 42%. More and more people are relying on online stores to make their purchases as a greater part of Indonesia’s population are in their 30s and busy with daily work.

Another great development in the retail landscape of Indonesia is that modern retailing is not only concentrated in its capital city. Malls, supermarkets and convenience stores are spreading significantly throughout the East Java, North Sumatra and North Sulawesi as well.

The evident growth in Indonesia’s retail sector is characterized not just by high rise buildings of retail stores and the growing numbers of convenience stores in every street. It can also be reflected upon the consumer spending, consumer behavior and trend which relates to the population being more inclined on imported brands. As retail sales figures continue to soar high, Indonesia is a promising place for foreign investors. The modern retail sector in the country holds huge potential for consistent growth. Competition among retail channels will also encourage further expansion among major retailers. However, it is certain that modern retail will continue to prevail and will soon dominate the market share in Indonesia as the income of people increases along with the demand for convenience.

When people talk about convenience and quality of services, we can definitely give it to the Japanese people. They know the value of not just money, but also people’s time. That’s why convenience stores or “konbini” as what it is locally referred to definitely takes our definition of a “one-stop shop” to a whole new level.

More than 50,000 convenience stores can be found in Japan. Every street corner even to the most provincial places has convenience stores. It’s where people usually go to purchase their food or simply to have coffee and have a rest from the cold outside. There is a fierce competition among major convenience stores operators in Japan such as 7/11, Family Mart and Lawson. This competition enables them to come up with innovations and creations of products to make the experience truly convenient for their consumers.

Each store has a wide variety of ready to eat food. For most Japanese people who just wants to grab something to eat because of their busy schedule, convenience store is definitely the place where they go to. Besides the fact that it’s a fast purchase, ready to eat food in convenience stores doesn’t lack the quality and good taste other restaurants also offer. Though most foods offered are Japanese, there are also Western food like pasta and sandwiches that can be purchased. The store clerk will always offer to reheat the food.

Other items such as cold beverage, ice creams, packed biscuits and snacks, alcoholic beverage and other food items can be found in convenience stores. These products also change depending on the season.

Besides food items, personal care products, cosmetics, batteries and other basic necessities can also be bought inside the convenience stores. Books, manga series, newspapers, magazines, and umbrellas are also available.

It’s hard to hail a cab on some places in Japan, most especially outside city centers. That’s why most convenient stores in these areas have a phone that a person can use to call a cab. Aside from this, these convenience stores also have public restrooms that people can use.

ATM Machines can also be found inside the convenience stores. Besides the banks, people go to convenience stores to withdraw their money from their ATM Cards. Branches of 7/11 have ATM Machines where international ATMs such as visa and mastercard can be accepted and used to dispense Japanese yen.

Multi-copy machines can also be used inside the convenience stores. But instead of the typical photocopier, they can also be utilized to send fax mails, print digital pictures and print documents from flash drives.

Another innovative machine found on Japanese Convenience stores is what they call the Loppi Machines. These red-colored machines can be used to buy tickets on various events in Japan such as concerts, sports, theme parks or even travel services. Once the machine dispensed the ticket, it can be paid directly to the counters. Besides tickets, the multi-purpose machine can also be used to confirm purchases made online or simply for bills payment (i.e. utility bills, insurance bills, cellphone bills). Loppi Machines make payments very easy as it can be made in many convenience stores. However, some machines don’t have an English Interface making it hard for foreigners to operate. Despite this, one can always ask assistance from the store clerk and they would be more than willing to help.

Finally, as most public places in Japan, convenience stores also offer free wifi access for a limited number of hours. For people passing by who need a drink and a place to rest, specifically tourist who also need the internet for directions, the stores’ free wifi access is truly convenient.

Japanese convenience stores truly offer its consumers not just good quality of purchases but also a worthy shopping experience. It redefines “convenience” to a level where consumers will not just find it easy to shop, but also to transact on most day to day necessary services. These stores, despite their size and assortment, would really come in handy for people, Japanese and Foreigners alike.