Download your copy here: https://web.tresorit.com/l/ocrzU#KqzMYrOBjt610PTn5Ta_0A

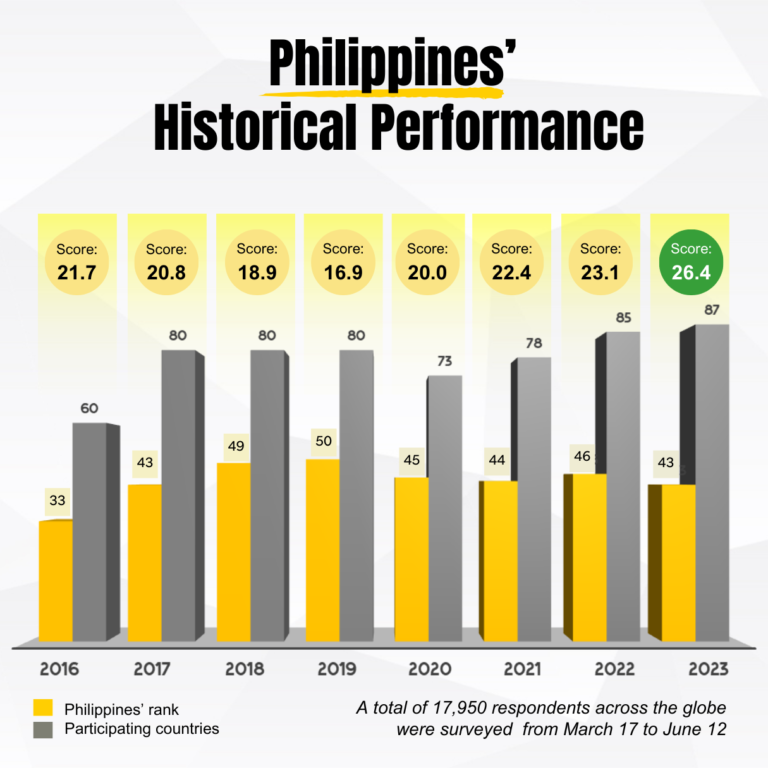

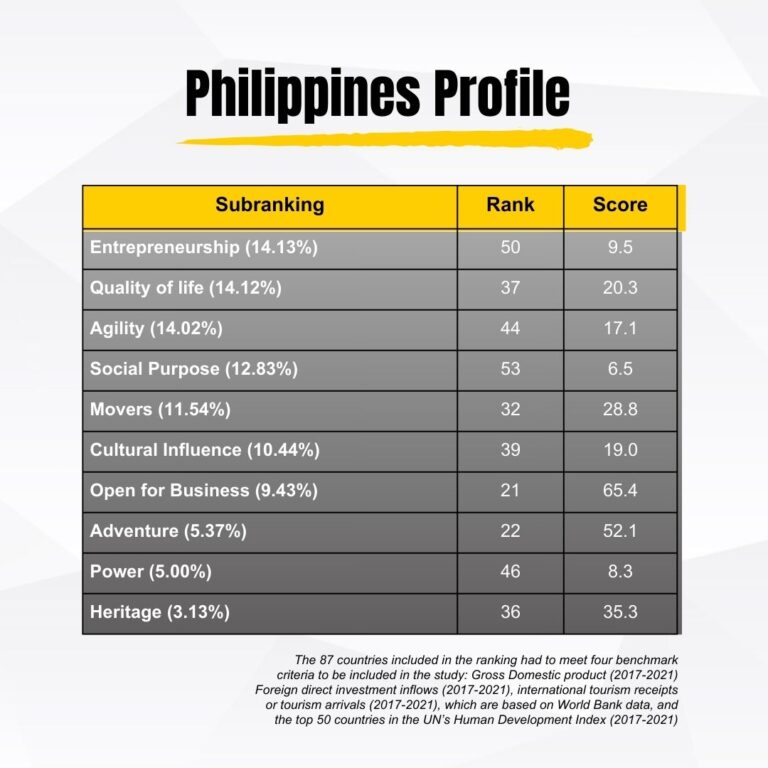

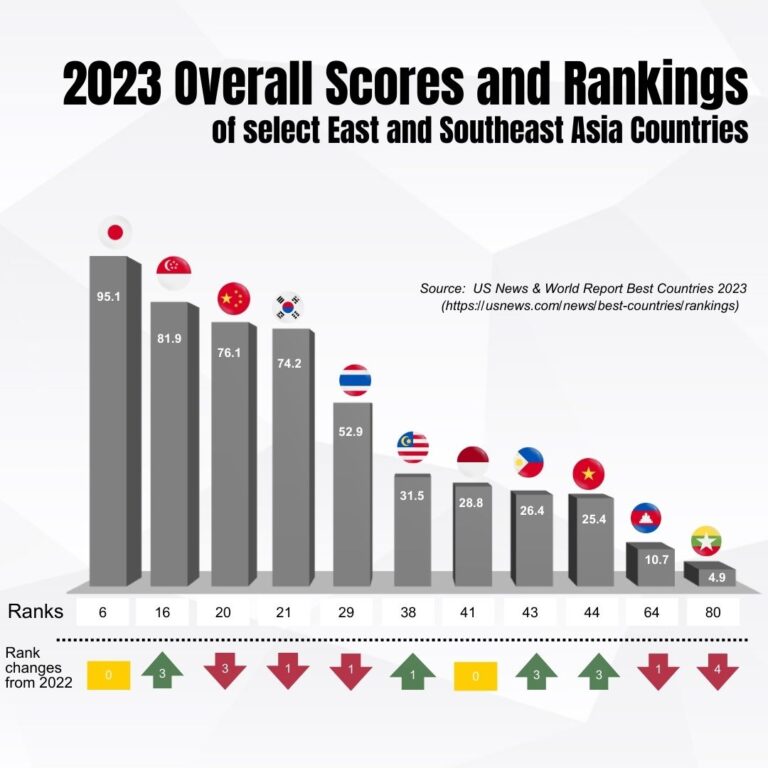

The Philippines climbed three spots to 43rd out of 87 countries with an overall score of 26.4 (out of possible 100) in the latest annual rankings of Best Countries by US News and World Report. The report ranks the countries based on how the world perceives them in terms of qualitative characteristics — impressions that have the potential to drive trade, travel, and investment, and directly affect national economies. Despite the improvement in its placement in the rankings this year, the Philippines placed the fourth lowest in the region.

Original Article: https://www.bworldonline.com/infographics/2023/09/26/547760/phl-rises-in-best-countries-list/

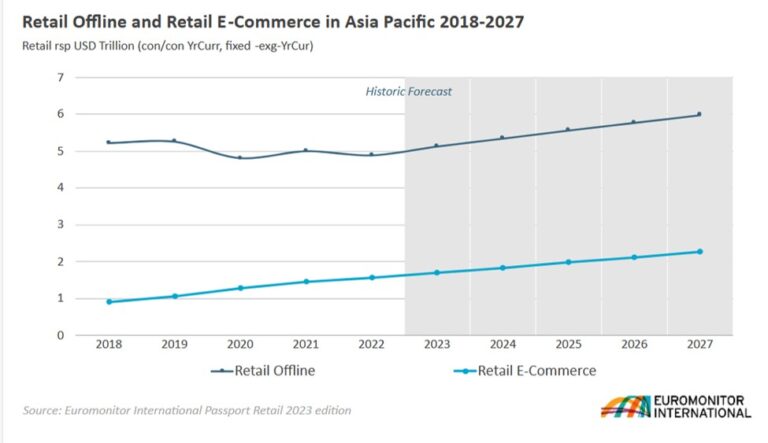

The impact of the pandemic on retail sales across markets in Asia Pacific varied greatly in 2022. The impact was largely dependent on each country’s COVID-19 situation, containment measures adopted, and the approach taken towards an endemic future.

Retail offline sales slumped in China by 4%, in absolute dollar terms, as lockdown policies contributed to a decline in in-store foot traffic. Conversely, markets such as India (+14%), Indonesia (+10%) and South Korea (+4%) experienced healthy growth and revenge spending due to the resumption of pre-pandemic lifestyles and social activities. Retail channels such as apparel and footwear specialists, beauty specialists and vending benefited from the recovery of international travel and geographic mobility of consumers.

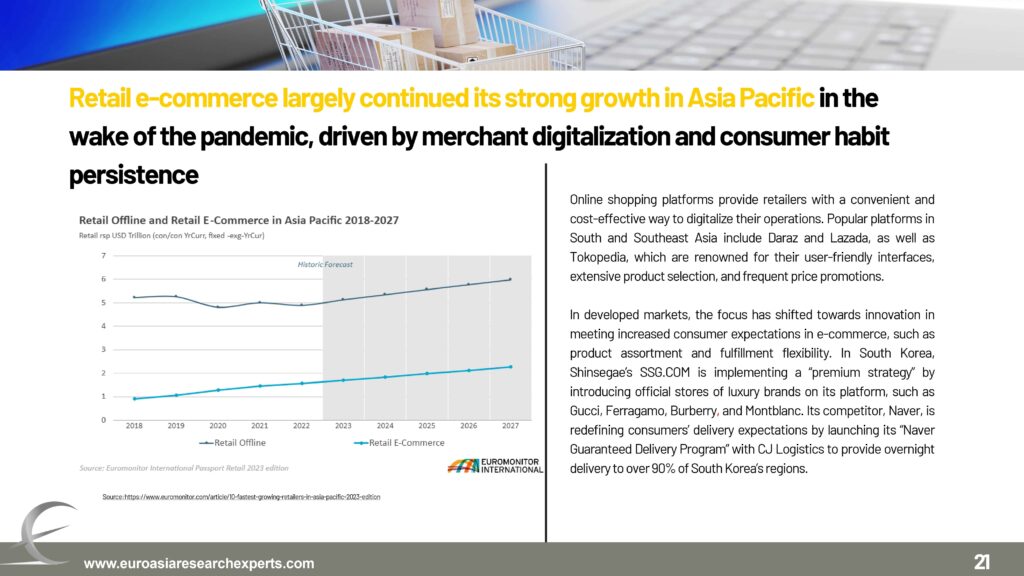

Retail e-commerce largely continued its strong growth in Asia Pacific in the wake of the pandemic, driven by merchant digitalisation and consumer habit persistence

The wide disparity in e-commerce development across Asia Pacific has resulted in differing strategic priorities and initiatives by brands and retailers.

Across developing Asia, e-commerce marketplaces offer a convenient and accessible option for retailers in their digitalisation journey. Platforms such as Daraz, Lazada and Tokopedia are popular among consumers in South and Southeast Asia due to their ease of use, wide product range and regular price promotions.

In developed markets, the focus has shifted towards innovation in meeting increased consumer expectations in e-commerce, such as product assortment and fulfilment flexibility. In South Korea, Shinsegae’s SSG.COM is implementing a “premium strategy” by introducing official stores of luxury brands on its platform, such as Gucci, Ferragamo, Burberry and Montblanc. Its competitor, Naver, is redefining consumers’ delivery expectations by launching its “Naver Guaranteed Delivery Programme” with CJ Logistics to provide overnight delivery to over 90% of South Korea’s regions.

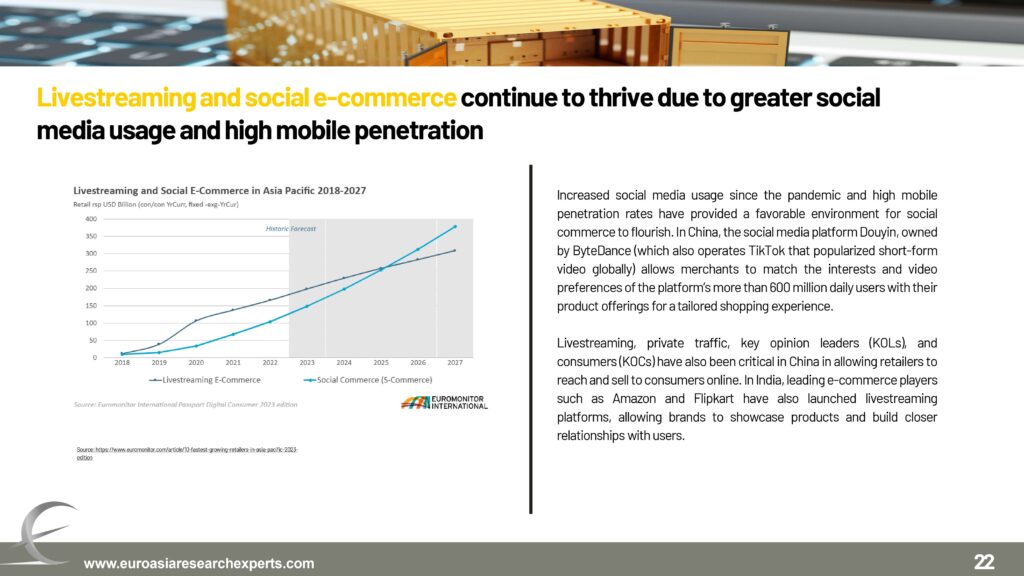

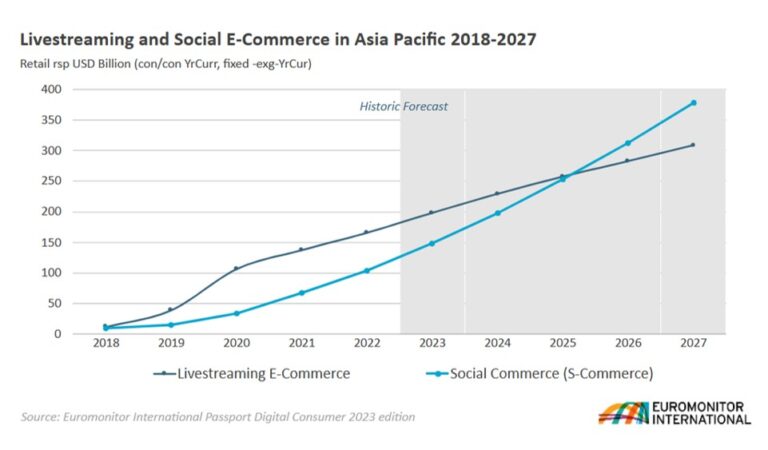

Increased social media usage since the pandemic and high mobile penetration rates have provided a conducive environment for social commerce to flourish. In China, social media platform Douyin, owned by ByteDance (which also operates TikTok and popularised short-form video globally) allows merchants to match the interests and video preferences of the platform’s more than 600 million daily users with their product offerings for a tailored shopping experience.

Livestreaming, private traffic, key opinion leaders (KOLs) and consumers (KOCs) have also been critical in China in allowing retailers to reach and sell to consumers online. Similarly in India, leading e-commerce players such as Amazon and Flipkart have also launched livestreaming platforms, allowing brands to showcase products and build closer relationships with users.

Consumers have returned to stores post-pandemic to find revamped outlet concepts that showcase the relevance of the physical store.

Experiential retail is taking centre stage as brands highlight their stores as more than a place to transact, but also a place where consumers can indulge in unique and memorable shopping experiences

Technology is also being used for a more customer-centric purchase experience in-store. Watsons’ “The Grand Store” in The Philippines utilises artificial intelligence (AI) and augmented reality (AR) as in-store tools to help consumers analyse their skin conditions or virtually try on cosmetics, helping consumers to find the most suitable products and be more confident in their purchase decisions.

COVID-19 has slowed down the pace of life and shone a spotlight on personal health and wellness, driving sustained sales through pharmacies and health and personal care stores. Preference for sustainable products has also grown, with retailers similarly placing greater emphasis on addressing environmental concerns through consumer education and in their retail operations. For example, AEON Group in Japan opened a store which runs on 100% renewable energy, with the aim for this concept to expand, and an end goal of achieving zero aggregate CO2 emissions from its stores by 2040.

The post-pandemic Asia Pacific retail landscape remains competitive. There has never been a greater array of choices across physical and digital channels, and technology and online tools will continue to transform the way retailers engage and sell to consumers. Retailers across the region are certainly facing new and unprecedented challenges, but those that are able to turn these challenges into opportunities are well-placed to remain the preferred shopping destinations of consumers.

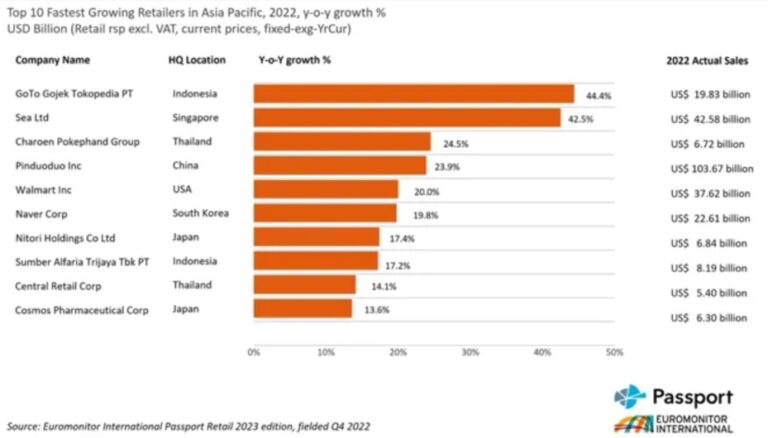

Sea Ltd ranked second in our list of fastest growing retailers in Asia Pacific, with sales growth of 43% y-o-y in 2022. According to Euromonitor International’s Retail research, Sea Ltd achieved USD43 billion in retail value sales in Asia Pacific in 2022.

Shopee is Sea Ltd’s flagship mobile-first e-commerce marketplace, which operates across seven Asia Pacific countries. It offers products in major categories from both third party merchants and official brand-owned e-stores, such as Shopee Mall.

Shopee is best known for its monthly sales and super brand days (exclusive partner-brand 24-hour sale events where the brand’s products highlight discounts, promotions and occasionally exclusive launches). It differentiates itself via its hyper-localised sites and marketing campaigns, competitive pricing and extensive product range. The Shopee app also includes livestreaming capabilities and interactive games (such as Shopee Farm) to drive consumer engagement.

Shopee is an attractive destination for third party merchants seeking to reach millions of e-commerce consumers across Southeast Asia and Taiwan, due to its high brand awareness and strong merchant support in driving sales via marketing and consumer engagement tools. Shopee has also expanded into adjacent services, such as food delivery and payments, to encourage continuous consumer reliance and spending on its platform.

Nitori is a leading home products specialist hailing from Japan. The retailer internally manages its vertical supply chain, which allows it to control an entire process from planning, manufacturing, distribution and retail, ensuring product quality and minimising external costs incurred.

The retailer has constantly expanded its footprint outside of Japan to markets such as Mainland China and Taiwan. In 2022, it opened its first outlets in Southeast Asia, in Malaysia and Singapore. Southeast Asia is home to the steady demand for homewares and home furnishings due to healthy economic growth and increase in number of households. Nitori has adroitly identified this opportunity in a rather fragmented industry.

Nitori plans to accelerate further penetration in overseas markets with 77 new outlets in the pipeline to open in the new fiscal, including entering other Southeast Asian countries, such as Thailand and Vietnam, where the retailer has operated production facilities for nearly two decades.

Original Article: https://www.euromonitor.com/article/10-fastest-growing-retailers-in-asia-pacific-2023-edition

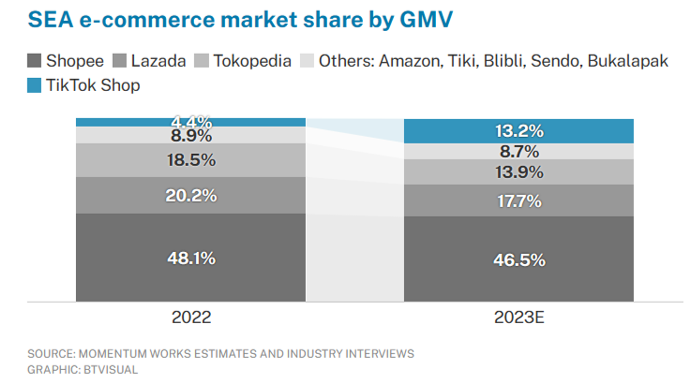

This will make it the fourth-largest e-commerce player in the region by gross merchandise value (GMV), behind Tokopedia with 13.9 per cent, Lazada at 17.7 per cent, and Shopee, which is set to top the market with a 46.5 per cent share of GMV.

The consultancy said this market share estimation is based on two factors – that TikTok reaches its GMV target of US$15 billion in South-east Asia in 2023, and that the other e-commerce players continue to see growth rates similar to 2021 and 2022.

In a report on Monday (Aug 21), Momentum Works noted that TikTok Shop has shown “impressive” growth in South-east Asia, and the region also makes up most of its global GMV. TikTok Shop’s business grew from US$0.6 billion in GMV in 2021 to US$4.4 billion in 2022, and is set to reach a US$15 billion target in 2023.

“This will put TikTok Shop in the same league as established players Lazada and Tokopedia,” Momentum Works said.

The consultancy derived its data from interviews with platforms, logistics and payment players in each country in the region, as well as consumers and other ecosystem stakeholders. These were then cross-checked with numbers disclosed by platforms and calibrated to obtain the final numbers.

The report’s coverage of e-commerce included key marketplaces such as Shopee, Lazada and TikTok Shop, and excluded brands’ own platforms in the online retail market.

TikTok Shop has operations in all major South-east Asian markets – Singapore, Indonesia, the Philippines, Vietnam, Malaysia and Thailand – as well as in the UK, US and Saudi Arabia.

Momentum Works highlighted four characteristics of TikTok Shop that distinguish it from other e-commerce players.

First, unlike standalone e-commerce apps, TikTok Shop is an in-app feature of a social media platform. This means that it enjoys natural traffic via TikTok, which exceeded one billion monthly active users globally in 2022. This helps TikTok Shop save on costs to acquire and retain users.

Second, TikTok’s e-commerce sales are also mainly driven by recommending content to its users, in contrast to conventional marketplaces where users search for products.

Third, the platform is content-driven, with creators and multi-channel networks playing vital roles in the ecosystem.

Fourth, TikTok Shop does not have payment and fulfilment infrastructure, although it is working in that direction. Reuters reported earlier this month that TikTok is in the process of obtaining a payment licence in Indonesia.

In China’s e-commerce market, TikTok’s sister company Douyin and Chinese agriculture-focused online retailer Pinduoduo are already making waves. Within six years of their moving into the market, Alibaba’s market share had shrunk from more than 80 per cent to less than 50 per cent, according to Momentum Works.

While TikTok Shop is fast emerging as a serious contender against incumbent e-commerce majors such as Shopee and Lazada in South-east Asia, Momentum Works also sees TikTok competing with Amazon in the US and Middle East.

“Ultimately, change is the only constant. Whether TikTok Shop is a threat to incumbent platforms might not be a standalone question at all,” said Weihan Chen, Momentum Works’ insights lead.

“The bigger narrative is that in e-commerce, where leading players seem to have a network effect and structural advantage, disruption can still happen, and the incumbents should always remain focused and vigilant.”

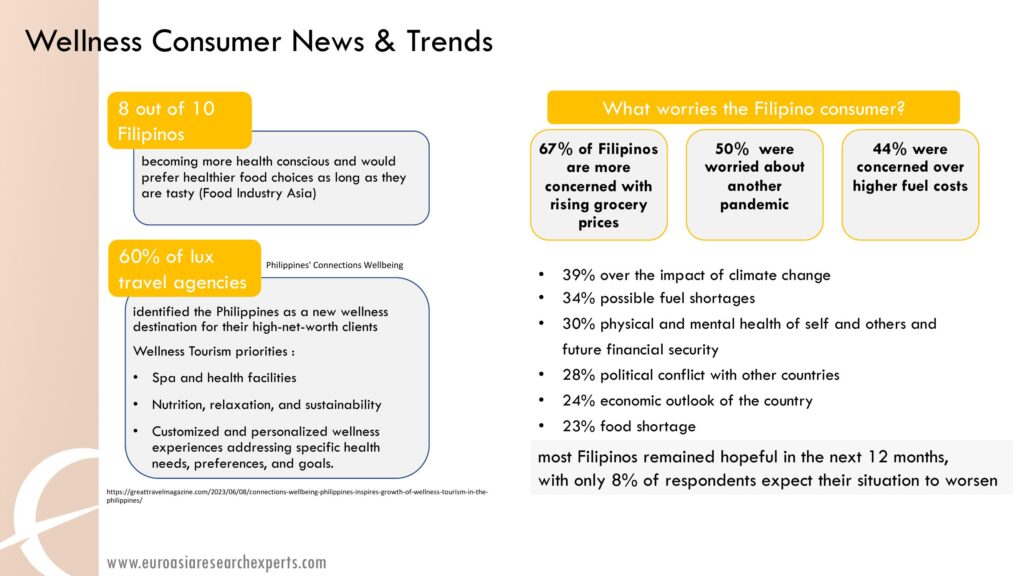

ALMOST SEVEN out of 10 Filipinos are more worried about rising grocery prices than the possibility of another pandemic, a report by marketing data and analytics company Kantar showed.

“When we asked our respondents what concerns them most, top of the list and on top of their minds would be rising grocery prices… They’re even more scared of the rising grocery prices over another pandemic crisis from happening again,” Laurice Padlan-Obana, Kantar Philippines Worldpanel Division Consumer and Shopper Insight director, said during a virtual briefing on Wednesday.

Kantar’s Shopperscope 2023 report showed that 67% or seven out of 10 Filipinos are more concerned with rising grocery prices, while 50% were worried about another pandemic and 44% were concerned over higher fuel costs.

The survey used for the Kantar report was conducted from February to April and covered 2,000 households across the Philippines.

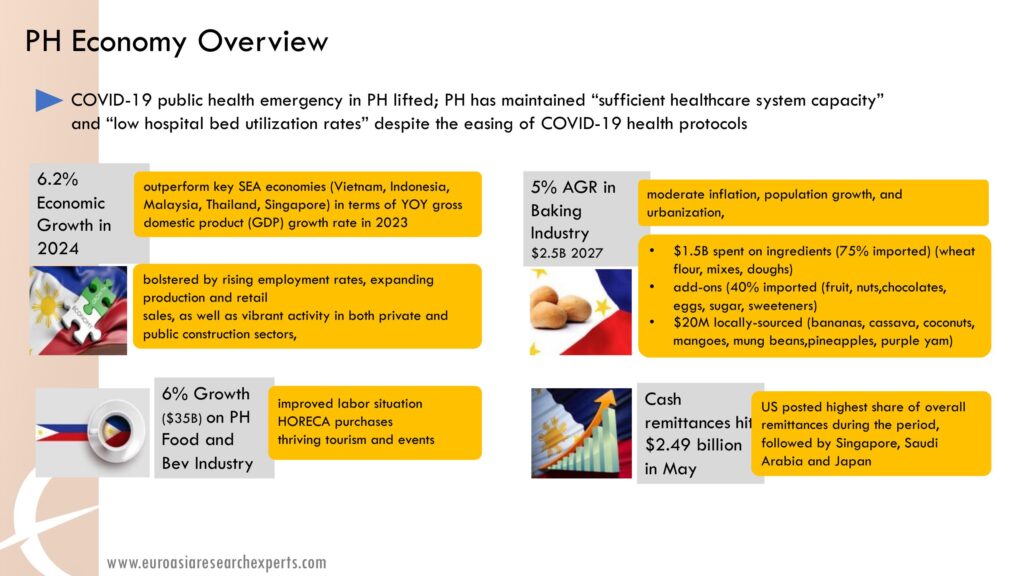

Inflation peaked at 8.7% in January, as prices of food and fuel continued to surge. Since then, the consumer price index slowed to 8.6% in February, 7.6% in March and 6.6% in April.

Kantar said Filipino consumers were also concerned over the impact of climate change (39%), possible fuel shortages (34%), physical and mental health of self and others (30%), future financial security (30%), political conflict with other countries (28%), economic outlook of the country (24%), and food shortage (23%).

However, most Filipinos remained hopeful in the next 12 months, with only 8% of respondents expect their situation to worsen.

Ms. Padlan-Obana said more Filipinos are putting more emphasis on price and affordability when choosing where to purchase grocery items.

Consumers are also looking for stores with longer hours and quick checkouts as they return to their regular routines, she added.

The Kantar report classified Filipino shoppers into three groups — “struggling” or those who are unable to cover their expenses; “managing” or people who finds ways to make both ends meet; and “comfortable” or those who have the least budget constraints.

“The ‘struggling’ are foremost concerned about rising prices and another pandemic happening. The ‘managing’ shoppers are concerned about the same things as struggling shoppers. The ‘comfortable’ are not only concerned about rising prices of goods but also about their health and their financial security in the future,” Ms. Padlan-Obana said.

She noted majority of Filipinos are those that can find ways to make ends meet, which means they have a lot of discipline when making purchases.

Ms. Padlan-Obana said fast-moving consumer goods brands and retailers should understand the shopping behavior and preference of these shopper groups.

All three shopper groups buy their grocery items at hypermarkets, supermarkets, groceries, sari-sari stores, convenience stores, drug stores, and direct sales, with varying levels of frequency and loyalty.

“The way to win them is communicating how they can save and maximize value in what they are paying for,” Ms. Padlan-Obana said.

The report also showed 68% of Filipinos plan their trips with a budget and grocery list. “Comfortable” shoppers also bring their families along during grocery shopping while “struggling” shoppers typically go by themselves.

“Shoppers go to hypermarkets and supermarkets in a purposive and deliberate manner. It is highly planned, going straight to the aisles to look for where items on their list are found,” Ms. Padlan-Obana said.

The report also showed Filipinos are visiting sari-sari stores more often, with a 5% annual increase to 212 trips. Nearly all or 99.7% of households buy from sari-sari stores, Kantar added.

MANILA, Philippines – Lucio Co’s Puregold Price Club is expanding its foothold in the Greater Manila Area through the acquisition of 14 stores of DiviMart supermarkets.

The deal will instantly convert all acquired DiviMart locations to Puregold under a sublease transaction.

These 14 stores are located in:

An additional 18 DiviMart locations will be evaluated for possible conversion to Puregold stores, according to Puregold’s stock exchange filing.

DiviMart is a Filipino supermarket chain founded in 1989 by Harry Uy and Vivian Ong Juanitas. It has over 30 branches nationwide and is known for its affordable goods.

Puregold told regulators that the acquisition is below 10% of the company’s book value.

“The parties are still finalizing the definite consideration for the contemplated transaction because the evaluation of store locations, improvements, furniture, fixtures, equipment, and merchandise inventory is still ongoing,” Puregold said.

As of end-March, Puregold had a total of 531 stores nationwide – 456 Puregold stores, 23 S&R Membership Shopping Warehouses, and 52 S&R New York Style QSRs.

Puregold’s consolidated net income went up 12% to P2.4 billion in the first three months of 2023.

Net sales for the first quarter rose by 15% P44.4 billion. Puregold Stores contributed P30 billion while S&R Warehouses contributed Php 14.4 billion. – Rappler.com

Pandamart, foodpanda’s online grocery store, has launched its first-ever physical pop-up store in the country. The new pandamart Pop-Up store is located in Trinoma Mall in Quezon City ready to serve consumers with its wide assortment of fresh, frozen, snacks, drinks, pantry essentials, pharmaceuticals, and other household items. Now shoppers can fully immerse themselves in the pandamart shopping experience.

The new pandamart pop-up store allows consumers to browse through the displayed products in the kiosk, order conveniently in the foodpanda app, and pick up the items

on the same day.

“The online grocery space is ever-growing and ever-changing, so to keep up with the current times, we are stepping up our game in offering a wide selection of quality groceries to customers,” said Danielle Eleazar, Head of Marketing (New Verticals) of foodpanda Philippines.

Apart from offering a leveled-up experience to consumers, the pandamart pop-up store is also bridging the gap between the usage of online and offline channels when it comes to grocery shopping for its app users.

Available until the end of May, pandamart’s pop-up store provides impressive features to give shoppers and consumers a first-hand experience of what pandamart has to offer.

Pandamart shoppers are in for a treat. Exciting activities, exclusive promos, discount vouchers, item giveaways from brand partners await pandamart shoppers; additional chances to win more prizes with the entertaining spin-the-wheel games. But wait, it doesn’t stop there! On May 27, tune in to the special Facebook live stream online selling event for a chance to win additional vouchers and prizes of up to Php 10,000!

Want to try foodpanda’s pandamart for the first time? Use the voucher code NEWGROCER for Php 100 off on your first order and enjoy convenient online grocery shopping in the comfort of

your home!

Global e-commerce spending will be led by millennials this year and they prefer online versus in-store when it comes to shopping.

Those are top findings from an ESW Global Voice survey that revealed more than 25% of millennials will spend more online this year when it comes to health, beauty, apparel, consumer electronics and luxury items.

The study also revealed nearly 73% of millennial shoppers plan to spend the same or more online in 2023, which will make this cohort the leader in global e-commerce spending this year, according to a press release on the findings..

“The millennial consumer remains fully committed to their preference for online shopping over physical retail,” Patrick Bousquet-Chavanne, president and CEO, ESW Americas, said in the release. “Millennials’ spending power has grown to $2.5 trillion, and they are not yet even in their prime earning years. They are spending more online than in-store across several categories, and these results indicate that brands must continue to evolve, improve, and optimize their e-commerce to attract and retain this increasingly powerful demographic.”

The survey’s polled more than 16,000 respondents across 16 countries comprised international shoppers across all demographics.

Additional findings include:

See the full report of ESW: https://esw.com/wp-content/uploads/2022/01/global_voices_2022.pdf