Out of the eight billion people in the world today, 64% use the internet, double the rate from a decade ago. Internet access has disrupted consumer life, including how they shop. Euromonitor International forecasts that consumers will spend nearly USD11 trillion on goods and services bought online in 2024.

This growing digital base needs to be at the center of your retail strategy. At NRF 2024: Retail’s Big Show in January, I spoke about the digital shopper trends that will have the biggest impact on retailers and brands. Let’s break down three big ones to watch in 2024.

Intuitive E-Commerce

The rising influence of digital channels is putting pressure on companies to improve the online experience. This is becoming possible due to evolving data-gathering strategies and emerging technologies, from AR to IoT to generative AI. These advances have the potential to transform the online shopping experience, leading to one that is more intuitive.

Consumers have greater expectations. About half of digital consumers want one-of-a-kind offerings. A fifth note the desire for more personalized shopping experiences. In both cases, these sentiments are higher among the most digitally savvy population, according to Euromonitor’s consumer research. That is telling as this shift toward a more intuitive experience is playing out on digital channels where these consumers shop more frequently.

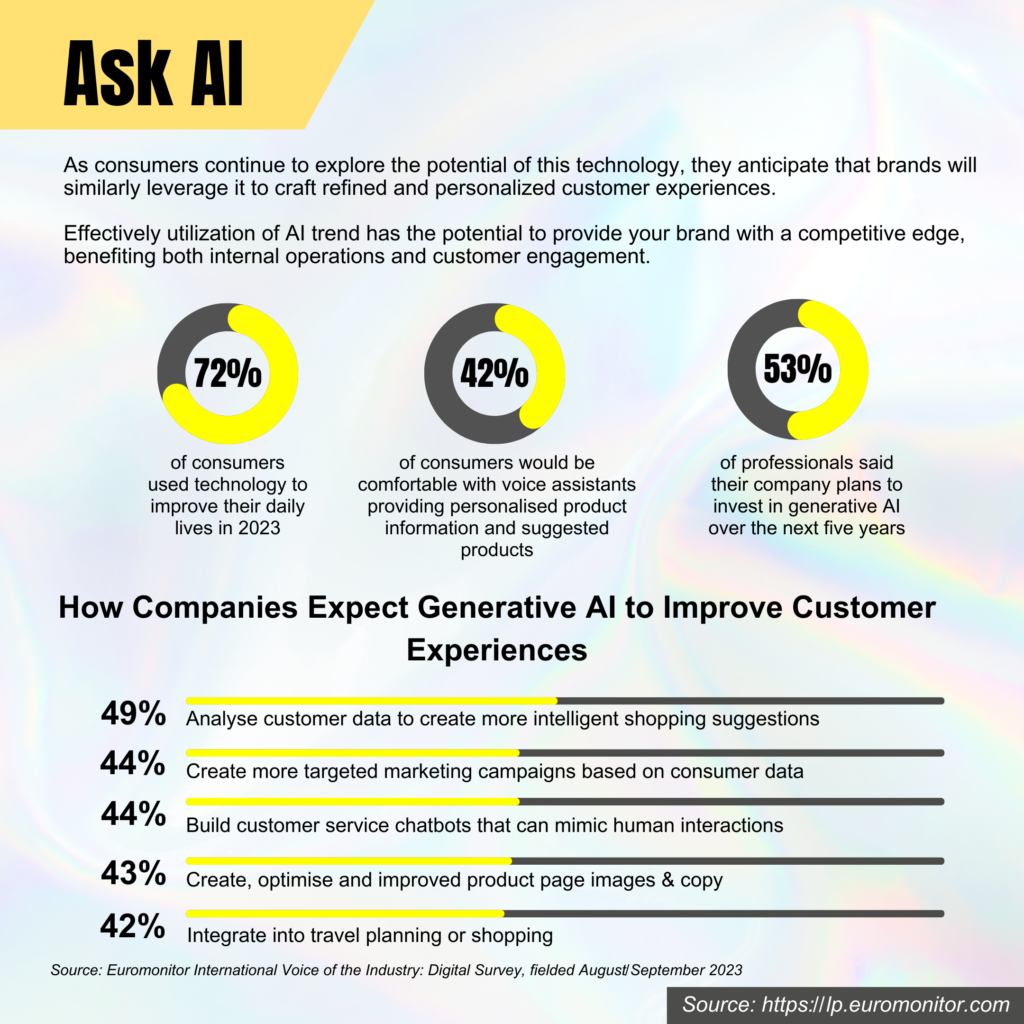

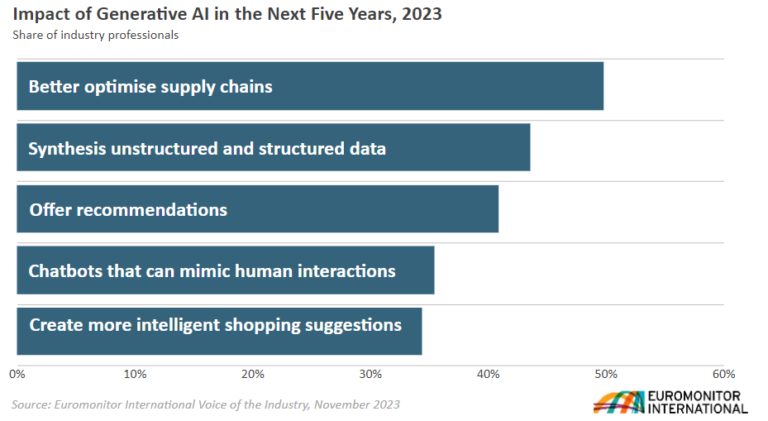

In part, this means ensuring the online channel is more akin to what a consumer might experience in person. While a variety of data and tech will be used, generative AI is poised to take on a central role in shaping the online experience. Generative AI can be leveraged in a variety of ways, from improving customer service to tailoring marketing messages to optimizing supply chains.

Virtual assistants powered by generative AI can create a more intuitive experience by using additional information sources for added context. Zalando’s new chatbot offers suggestions based on natural questions the shopper might ask, and in the future, could be combined with personal preferences, taking steps toward making the discovery experience feel more intuitive.

Almost half of industry professionals say they plan to invest in generative AI in the next five years

Source: Euromonitor’s Voice of the Industry Survey, 2023

New technologies like generative AI could give brands a competitive advantage. The pioneers who can create a next-generation shopping experience using these advances will be the ones that fuel a new shopping behavior and usher in the next so-called “Uber moment.”

TikTok Economy

Digital consumers are flocking to TikTok and its Chinese sister platform, Douyin. Brands are striving to promote their products and services on these platforms known for their short-form video content, but some of the viral trends that are doing the most to boost brand sales are emerging organically from users on those platforms.

These ByteDance platforms are not only some of the most popular, but also the fastest growing. As of 2023, 43% of digital consumers globally report using them monthly, a 19-percentage-point jump in three years, according to Euromonitor’s Voice of the Consumer: Digital Survey. These short-form video platforms, also known for their endless scroll and advanced algorithms, are a hit with young consumers, especially Gen Z.

Although most marketing campaigns on TikTok are financed or initiated by brands, some of the most viral content is organic. In 2023, an Israeli TikTok influencer posted a video of herself wrapping a frozen Betty Crocker Fruit Roll-Up processed snack around ice cream to create a crunchy fruit-flavored ice cream cone. Almost overnight, Fruit Roll-Ups began flying off shelves, creating a black market.

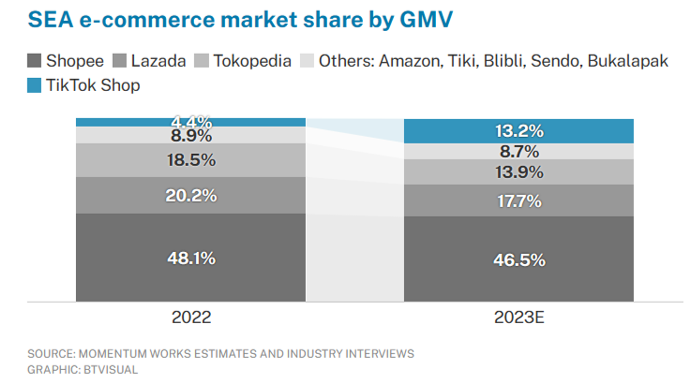

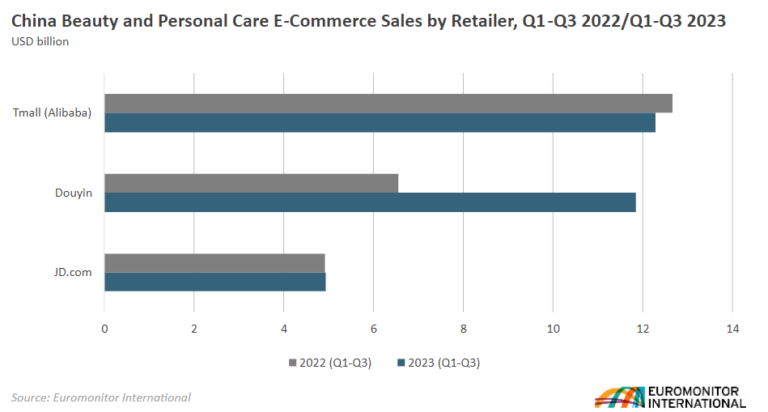

ByteDance platforms are dabbling in retail. In 2020, Douyin pivoted from being a pure social media platform to a retailer, prioritizing smaller sellers with a low-fee structure with revenue supplemented by advertising. Douyin has seen massive e-commerce gains. Online sales of beauty and personal care products on Douyin’s marketplace surged 81% in the first nine months of 2023, as compared with the same period in 2022, according to Euromonitor’s new e-commerce research. As for TikTok, its TikTok Shop is finding success in Southeast Asia and set up shop in the US and UK in September.

Revamped Returns

Consumers have long wanted hassle-free returns but delivering on that expectation has not been without challenges. The convergence of trends, like the rise of e-commerce, closure of stores by some retail chains and boost in sustainable strategies, is moving returns up the industry agenda. New technologies and partnerships are paving the way to a happier return experience for shoppers.

Creating a hassle-free return experience is not without challenges. First, what is deemed hassle-free varies by consumer. Although 43% of digital consumers point to mail as the preferred channel for online purchase returns, preferences vary by generation. For example, baby boomers prefer to return by mail, while Gen Z prefer to return in-store. To solve the unhappy return experience, the industry needs to shift its mindset, viewing this as being about improving loyalty, rather than a revenue drain.

Retailers are deploying a variety of tactics to reduce returns or at least their impact on the bottom line. Electronics specialist Best Buy is opening 10 smaller outlets, specializing in selling used and refurbished electronics. The aim of these stores is to target budget-conscious shoppers and recoup more from open-box and return products. More and more retailers are outsourcing the return experience to companies like Happy Returns or Loop Returns, which provide merchants with a customizable online portal for returns and exchanges.

To date, many retailers have struggled to grasp the pivotal role returns play in shaping customer loyalty and, as such, have sidelined this moment. That’s changing.

Two-thirds of retail professionals said they plan to continue or even accelerate investment in product returns

Source: Euromonitor International’s Voice of the Industry: Retail Survey

Looking ahead

These trends demonstrate how online shopping continues to mature, improving the customer experience from the moment of discovery to potential product return. A second, prominent theme is how consumers desire more power in their relationship with brands. TikTok Economy is rooted in how consumers are using social media to gain power in the value exchange. This power has led to more authentic messaging, which resonates with younger consumers like Gen Z.

As you begin to execute your 2024 strategy, use these insights to guide your campaigns, decisions and growth plans with the most digitally savvy consumers.